Key takeaways

- Form FC-TRS is the RBI reporting form used to record transfers of capital instruments between residents and non-residents under FEMA.

- FC-TRS must be filed through the RBI FIRMS portal within 60 days of the transfer or fund movement, whichever is earlier. The process involves user registration, form submission, and verification by the Authorised Dealer (AD) bank.

- All transfers must follow FEMA pricing guidelines. When a resident sells to a non-resident, the price must not be below fair value. When a non-resident sells to a resident, the price must not exceed fair value.

- If the filing is delayed, the company must regularise the delay by paying a Late Submission Fee (LSF) as prescribed by the RBI before the form can be approved.

- Common reasons for FC-TRS rejection include outdated valuation certificates, mismatches in shareholding data, and incomplete remittance documentation. Aligning all documents before submission reduces the risk of queries from the AD bank.

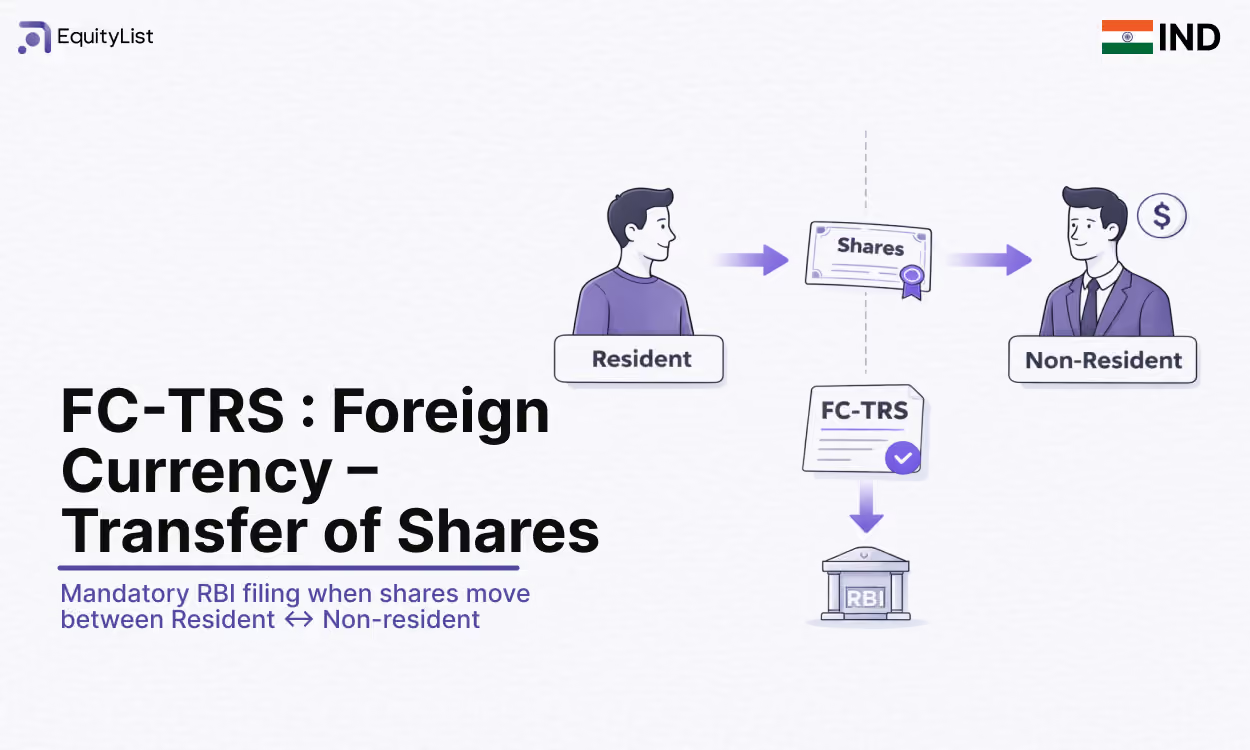

What is FC-TRS?

Form FC-TRS (Foreign Currency – Transfer of Shares) is the RBI regulatory form used to report the transfer of capital instruments between a person resident in India and a person resident outside India.

The reporting requirement arises under the Foreign Exchange Management Act, 1999 (FEMA) and the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019.

For example, consider a situation where FC-TRS becomes applicable: a secondary sale to a foreign investor.

- An Indian startup founder sells 1,00,000 equity shares to a US venture capital fund.

- Transfer price: ₹150 per share

- Total transaction value: ₹1.5 crore

- The shares are transferred through a share purchase agreement and payment is received through authorised banking channels.

Since the transaction involves a transfer of shares from a resident to a non-resident, it must be reported to the RBI using Form FC-TRS.

When is FC-TRS filing required?

FC-TRS applies when existing capital instruments are transferred between a resident and a non-resident. The capital instruments covered, including:

- Equity shares

- Compulsory Convertible Preference Shares (CCPS)

- Compulsory Convertible Debentures (CCD)

- Share warrants

- Other capital instruments as defined under the NDI Rules

Unlike FC-GPR, which applies to fresh issuance of capital instruments, FC-TRS applies to secondary transfers where ownership of existing securities changes between a resident and a non-resident.

FC-TRS may also be required when a non-resident transfers shares to another non-resident, unless the transfer falls within the exempt categories under FEMA. In certain sectors, such transfers may additionally require government approval under the FDI policy.

Each transfer transaction must be reported separately. In case multiple transferors or transferees are involved, separate filings may be required for each transfer leg.

When is FC-TRS not required?

FC-TRS is not required in the following scenarios:

- Transfer between two persons resident in India.

- Transfer from a non-resident holding capital instruments on a non-repatriable basis to a resident, and vice versa (these are treated as domestic transactions for reporting purposes).

- Transfer between two non-residents both holding capital instruments on a repatriable basis (as the repatriation status does not change).

- Transfer of capital instruments by way of gift (gift transfers have a separate reporting process and are not filed through FC-TRS by way of sale).

- Fresh issuance of capital instruments to a non-resident, which is reported through FC-GPR.

Who is responsible for filing FC-TRS?

The responsibility to file Form FC-TRS lies with the Indian resident party involved in the transaction. This could be either:

- the resident seller (transferor), or

- the resident buyer (transferee)

In certain cases, a non-resident holding shares on a non-repatriable basis may also be required to file the form.

Note: An investment on a non-repatriable basis means the investor cannot freely send the sale proceeds outside India. These investments are typically made through NRO (Non-Resident Ordinary) accounts and are treated differently under FEMA.

Conversely, an investment on a repatriable basis means the investor can freely remit the sale or maturity proceeds outside India, typically through an NRE (Non-Resident External) account. The repatriation status affects reporting and compliance requirements, and must be correctly disclosed when filing FC-TRS.

In case the shares are acquired by non-resident investors on the stock exchanges under the Foreign Direct Investment (FDI) scheme, reporting is done by a person resident outside India with Authorised Dealer (AD) category-I bank.

Documents required for FC-TRS filing

The documentation required for FC-TRS depends on whether the transfer occurs for consideration (sale) or without consideration (gift).

In case of sale

For a secondary sale transaction between a resident and a person resident outside India, the following documents are typically required:

- Board resolution approving transfer

- Form SH-4

- Shareholding pattern (before and after transfer)

- Share purchase agreement

- Consent letter from buyer

- Consent letter from seller

- Declaration by non-resident transferee

- Valuation certificate not older than three months

- Foreign Inward Remittance Certificate (FIRC) or bank remittance certificate

- KYC of foreign investor

- Press Note-3 Declaration as per Consolidated FDI Policy

In case of gift

Transfers without consideration are subject to stricter scrutiny under FEMA. The following documents are generally required:

- Name and address of transferor (donor) and the transferee (donee)

- Relationship between transferor and the transferee

- Reason for gift

- Valuation certificate

- Undertaking regarding USD 50,000 annual limit

- Copy of executed gift deed

- Sectoral cap compliance certificate

How to file FC-TRS on RBI FIRMS portal

FC-TRS filing requires a user account, which gets approval from the RBI. Once the account is activated, the authorised user can log in, fill in the FC-TRS form, upload the required documents, and submit the filing through the system. Once submitted, the form is routed to the AD bank for verification and approval.

Here’s how the complete FC-TRS filing process works:

Step 1: Create an ‘Entity User’ on the RBI FIRMS Portal

Before filing FC-TRS, the company must create an Entity User on the RBI FIRMS portal. This step registers the company in RBI’s reporting system. During registration, the following information must be provided:

- CIN and company details

- Company email and mobile number

- PAN

- Authorisation Letter on company letterhead

Once the registration request is submitted, the RBI reviews the application. If the details are approved, login credentials are sent to the registered email address. If the application is rejected, the identified issues must be corrected and the registration request must be submitted again.

Step 2: Register entity and create a ‘Business User’

After logging in as the Entity User, the company must first be registered under the Entity Master on the FIRMS portal. Once the entity is registered, an application must be submitted to create a Business User, who will be authorised to file forms such as FC-TRS.

2A. Register under Entity Master

Enter basic company details such as:

- CIN and address

- National Industrial Classification (NIC) code (select the primary business activity)

- Paid-up capital (on fully diluted basis)

If this is the company's first foreign investment, enter zero in the previous foreign investment fields.

The form does not allow draft saves, so all details must be prepared before submission.

2B. Create a Business User

The Business User account is required to file FC-TRS. To create it, you must:

- Fill details of the authorised person

- Select the correct AD bank

- Upload a Business User Authorisation Letter

After approval (usually within a few working days), you will receive login credentials. Once activated, the Business User can proceed to file FC-TRS.

Step 3: Initiate the FC-TRS filing

Once your Entity User and Business User are approved, log in to the FIRMS portal as the Business User. From the dashboard:

- Navigate to Single Master Form (SMF)

- Select FC-TRS

- Click on ‘Add New Return’ to initiate a fresh filing

If your company has previously filed forms such as FC-GPR or an earlier FC-TRS, you may be required to enter the earlier acknowledgement number. This helps RBI and the AD bank correlate the current transfer with past filings and maintain continuity in records.

After initiating the return, the FC-TRS form screen will open, and you can begin entering transaction details.

Step 4: Enter transfer and transaction details

The form requires disclosure of the following transaction particulars:

- Transfer by way of (sale or gift)

- Transfer from (buyer and seller as per their residential status)

- Transfer type as per FEMA classification

- Date of transfer

- Nature of transfer (private arrangement, offer for sale in IPO/FPO etc.)

- Details of buyer and seller

The date of transfer must align with the executed Share Transfer Deed, Share Purchase Agreement, or other relevant transaction documents.

Step 5: Enter capital instrument details

Capital instrument details that must be disclosed in the form include:

- Type of capital instrument (Equity Shares, CCPS, CCDs, etc.)

- Number of instruments transferred

- Conversion ratio

- Equity shares on fully diluted basis

- Face value

- Transfer price per instrument

- Total consideration amount

- Fair value (as per valuation certificate)

If the instruments are convertible, the instrument quantities must align with the fully diluted position where applicable. All numerical values must match supporting documents.

Step 6: Enter remittance details

Remittance details are not applicable in case of gift transfer.

In case of sale, you must disclose where the resident party received the funds (if selling securities) or from which bank account the payment was made (if purchasing securities), and confirm that the transaction took place through authorised banking channels. Accordingly, you will need to provide:

- Mode of payment (banking channel)

- Name and branch of AD bank

- Amount received/remitted in Rs.

- Whether remittance was received in multiple tranches

- FIRC/debit statement

- KYC attachment (foreign entity)

If payment was made by a third party on behalf of the investor, details of both the remitter and the investor must be disclosed. The remittance date must match the bank statement. All supporting documents must be properly signed, legible, and combined in the format required by the portal.

Step 7: Submit the form

All numerical entries, valuation figures, remittance dates, and shareholding calculations must be verified before submission.

After submission, the form is routed to the AD bank for scrutiny. The AD bank may approve the form, raise a resubmission request seeking clarification or corrections, or reject the filing, citing discrepancies

If a resubmission is raised, corrections must be made within the stipulated timeline. Once the AD bank approves the filing, the FC-TRS reporting process is complete.

What is the deadline for FC-TRS filing?

FC-TRS must be filed within 60 days from the date of transfer of capital instruments or the date of receipt or remittance of funds, whichever is earlier.

Late Submission Fee (LSF) for delayed FC-TRS

If FC-TRS is not filed within the 60-day timeline, the delay can be regularised by paying a Late Submission Fee (LSF) as prescribed in RBI circular RBI/2022-23/122.

LSF amount = 7,500 + (0.025% × A × n)

- A = Amount involved in the delayed reporting

- n = Number of years of delay, rounded upward to the nearest month and expressed up to two decimal points

The following additional conditions apply:

- The maximum LSF payable is capped at 100% of the amount involved (A) and is rounded upward to the nearest hundred.

- The option to pay LSF is available only up to three years from the original due date of filing.

- If LSF is not paid within 30 days from the date of advice issued by the RBI system, the advice becomes void. Any fresh application will reset the reference date for computing the delay period (n).

- If a person neither files the return within time nor regularises the delay through LSF, the matter may be liable for penal action under Section 13 of the FEMA, 1999.

Pricing guidelines for share transfer under FEMA

Pricing of share transfers between a person resident in India and a person resident outside India is governed by the FEM (NDI) Rules, 2019 and the RBI's Master Direction on Foreign Investment in India.

For FC-TRS filing, the applicable pricing rule depends on the direction of the transfer.

Transfer from a person resident in India to a person resident outside India

- Listed company: The transfer price must be determined in accordance with the applicable SEBI guidelines. In most cases, this means the price should be calculated using the preferential allotment pricing formula prescribed under SEBI regulations for the relevant period preceding the date of transfer.

- Unlisted company: The transfer price must not be lower than the fair value of the equity instruments. The fair value must be determined using an internationally accepted valuation methodology on an arm’s length basis and certified by a Chartered Accountant, a SEBI-registered Merchant Banker, or a practicing Cost Accountant.

Transfer from a person resident outside India to a person resident in India

- Listed company: The transfer price must be determined in accordance with the applicable SEBI pricing guidelines, typically based on the preferential allotment pricing formula for the relevant period preceding the date of transfer.

- Unlisted company: The transfer price must not exceed the fair value of the equity instruments certified by a Chartered Accountant, a SEBI-registered Merchant Banker, or a practicing Cost Accountant using an internationally accepted arm's length valuation methodology.

FEMA regulations do not permit assured exit prices for non-resident investors at the time of investment. When the shares are eventually transferred, the transaction must occur at the fair value prevailing at that time.

Pricing for convertible instruments

For convertible capital instruments such as CCPS or CCDs, the conversion price or formula must be determined at the time of issuance in accordance with FEMA pricing guidelines.

The conversion price cannot be lower than the fair value of equity shares determined at the time the convertible instrument was originally issued, in accordance with NDI Rules.

How conversion price works: The conversion ratio determines how many equity shares an investor receives for each CCPS or CCD held. It is calculated as:

Conversion ratio = Issue price of CCPS ÷ Conversion price

For example, if a CCPS is issued at ₹100 and the conversion price is ₹50, the ratio is 1:2. It means one CCPS converts into two equity shares. This ratio may also be adjusted for corporate actions such as stock splits or bonus issues to preserve the investor's economic position.

Common reasons for FC-TRS rejection by AD bank

During the review process, the AD bank verifies whether the transaction complies with FEMA, the FEM (NDI) Rules, and RBI reporting requirements. If discrepancies are identified in the form or supporting documents, the AD bank may raise a resubmission request or reject the filing. Common issues that lead to resubmission requests or rejection include:

- Valuation certificate older than three months at the time of filing

- Incorrect classification of repatriable or non-repatriable status of the investment

- Mismatch between the declared shareholding pattern and supporting records

- Missing or incomplete FIRC, KYC, or remittance documentation

- Sectoral cap breach under the applicable FDI policy

- Incomplete or missing declarations, including regulatory compliance declarations where required

- Incorrect selection of the capital instrument type in the FC-TRS form

The discrepancies may arise from inconsistencies between the information entered in the form and the supporting documentation. Ensuring that the valuation report, remittance records, transaction documents, and shareholding pattern are fully aligned before submission can significantly reduce the likelihood of queries or rejection by the AD bank.

What is the difference between FC-TRS and FC-GPR?

Both FC-GPR and FC-TRS are reporting forms prescribed under FEMA to track foreign investment in Indian companies.

While FC-TRS applies to transfer of existing capital instruments, FC-GPR is used for fresh issuance of capital instruments to a person resident outside India. Its purpose is to formally report new foreign capital inflows to the RBI.

Final thoughts

FC-TRS is a critical reporting requirement for secondary transfers involving foreign investors in Indian companies. FC-TRS reporting forms part of RBI’s framework for monitoring foreign investment transactions.

Because FC-TRS filings are scrutinised by Authorised Dealer banks and must comply with FEMA pricing rules, errors in valuation reports, remittance documentation, or shareholding disclosures can delay approval. Preparing documentation in advance significantly reduces the risk of resubmission requests or rejection.

FAQs

1. When is FC-TRS not required?

FC-TRS is generally not required for:

- Transfer between two residents

- Pure primary issuance of shares, which is reported through FC-GPR

- Transfer from a non-resident holding capital instruments on a non-repatriable basis to a resident, or vice versa

- Transfer between two non-residents both holding on a repatriable basis

2. Is FC-TRS required for rights issue?

No. Rights issue to a non-resident are treated as fresh issuance and reported under FC-GPR.

3. When is a valuation certificate required?

A valuation certificate is required in all transfers involving unlisted companies where pricing guidelines apply. The certificate must:

- Be issued by a Chartered Accountant, a SEBI-registered Merchant Banker, or a practicing Cost Accountant

- Use an internationally accepted methodology

- Not be older than 90 days from the date of the investment or transfer

For listed companies, if the pricing is determined strictly in accordance with SEBI regulations, a separate valuation certificate is not required. However, a Chartered Accountant's certificate confirming compliance with the relevant SEBI regulations must be attached to the FC-TRS filed with the AD bank.

4. What is a consent letter for FC-TRS filing?

A consent letter is a written confirmation from the buyer and seller acknowledging that they have agreed to the share transfer transaction. It typically states the number of shares being transferred, the agreed transfer price, and the identities of the transferor and transferee. The letter is submitted as part of the supporting documents during FC-TRS filing.