Key takeaways

- The SEBI SBEB Regulations, 2021 govern all share-based employee benefit schemes for listed companies in India, covering six scheme types: ESOS, ESPS, SAR, GEBS, RBS, and sweat equity.

- The 2021 regulations removed "permanent" from the employee definition, allowing non-permanent employees working exclusively for the company or its group to be eligible.

- Promoters, promoter group members, independent directors, and directors holding more than ten percent of equity are excluded from all schemes.

- Where a scheme involves secondary acquisition of existing shares, the trust route is mandatory; annual acquisition by the trust is capped at two percent of paid-up equity and the aggregate cap across ESOS, ESPS, and SAR schemes is five percent.

- Every scheme requires shareholder approval by special resolution. Additional resolutions are required for secondary acquisition, grants to subsidiary or holding company employees, and grants exceeding one percent of issued capital per individual per year.

- A minimum vesting period of one year applies to ESOS and SAR schemes. Death and permanent incapacity trigger immediate vesting.

- Issuance of sweat equity shares is capped at fifteen percent of paid-up equity per year and twenty-five percent in aggregate.

- The September 2025 amendment (Regulation 9A) permits founders classified as promoters in a DRHP to retain ESOPs granted at least one year before the IPO filing.

- The December 2025 amendment replaced merchant bankers with IBBI-registered valuers for sweat equity valuations, effective 2 January 2026.

The SEBI (Share Based Employee Benefits and Sweat Equity) Regulations, 2021, commonly called the SBEB Regulations, govern every equity-based compensation scheme offered by a listed company in India. If your company's shares are listed on a recognised stock exchange and you offer employees a scheme involving dealing in, subscribing to, or purchasing your securities, these regulations apply to you.

SEBI notified the regulations on 13 August 2021, consolidating two earlier instruments: the SEBI (Share Based Employee Benefits) Regulations, 2014 and the SEBI (Issue of Sweat Equity) Regulations, 2002. Two amendments followed in 2025, both covered at the end of this guide.

Scheme types covered by the SBEB Regulations

The SBEB Regulations apply to six scheme types, defined under Regulation 1(3):

- Employee Stock Option Scheme (ESOS): Employees receive the right to purchase company shares at a pre-determined price at a future date, a right but not an obligation. Shares are issued only when the employee exercises the option.

- Employee Stock Purchase Scheme (ESPS): The company offers shares directly to employees, either as part of a public issue or otherwise, for immediate purchase rather than a future right.

- Stock Appreciation Rights Scheme (SAR Scheme): Employees receive the right to receive appreciation in share value, calculated as the difference between the market price on the date of exercise and the base SAR price set at grant. Settlement can be in cash or equity. The SBEB Regulations specifically govern equity-settled SARs; cash-settled SARs fall outside their scope since no shares are issued.

- General Employee Benefits Scheme (GEBS): A scheme dealing in company shares for employee welfare purposes, including healthcare, disability, death benefits, and scholarships.

- Retirement Benefit Scheme (RBS): Company shares used to fund employee retirement benefits, subject to the same ten percent asset cap as GEBS.

- Sweat Equity Shares: Shares issued to directors or employees for providing know-how, intellectual property, or value additions. These are governed separately under Chapter IV of the regulations and Section 54 of the Companies Act, 2013.

Employee eligibility: Who qualifies and who is excluded

Regulation 2(1)(i) of SEBI (Share Based Employee Benefits and Sweat Equity) Regulations, 2021, defines "employee" for all schemes other than sweat equity. A key change from the 2014 regulations was the removal of the word "permanent," meaning non-permanent and contractual employees working exclusively for the company can now be eligible.

The definition covers:

- Employees designated by the company, working in India or abroad.

- Whole-time and part-time directors (excluding independent directors).

- Employees or directors of group companies, including subsidiaries, associate companies, and the holding company.

Who is excluded: Promoters, members of the promoter group, independent directors, and any director who holds more than ten percent of the company's outstanding equity shares, whether personally, through a relative, or through a corporate entity.

Where an identified employee is to receive grants equal to or exceeding one percent of issued capital in any one year, a separate shareholder resolution is required for that specific grant.

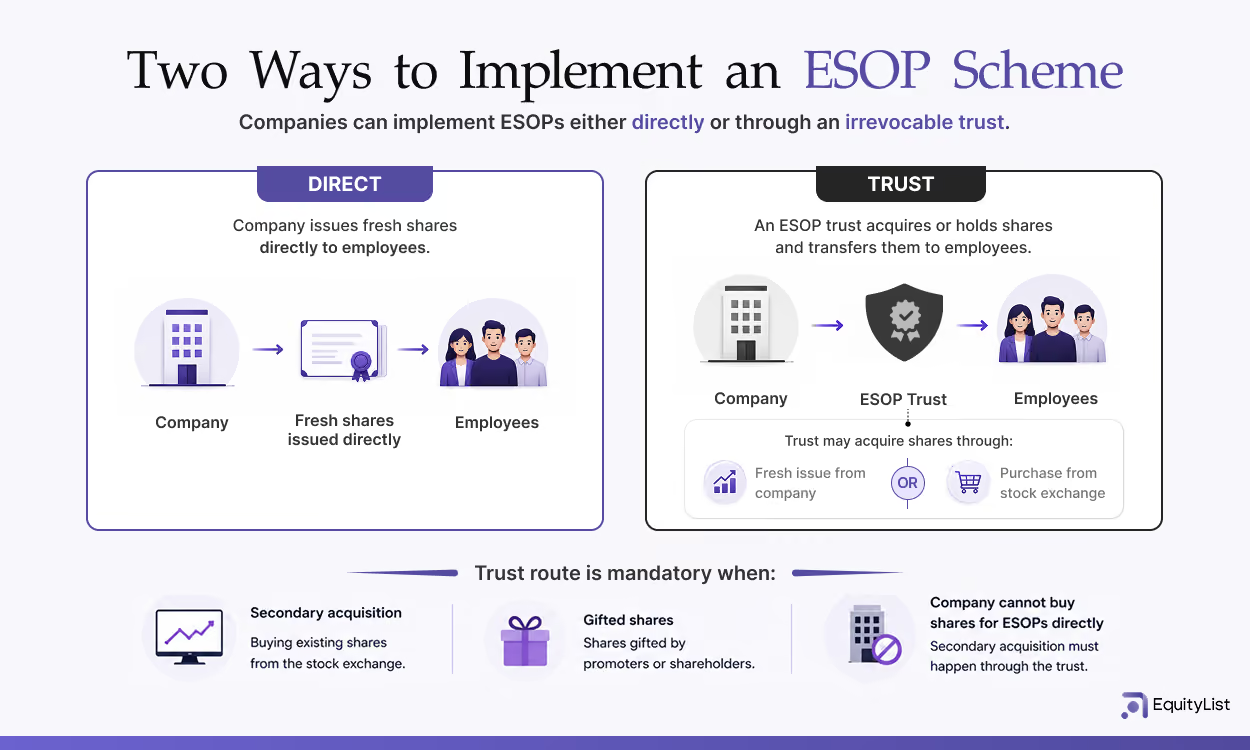

Direct route and trust route

A scheme can be implemented directly, by offering new shares to employees upon exercise, or through an irrevocable trust. The choice must be decided at the time of shareholder approval and can be changed with a fresh approval by shareholders through special resolution.

Where the scheme involves secondary acquisition, meaning purchasing existing shares from the stock exchange rather than issuing new ones, or involves gifting shares, the trust route is mandatory. Companies cannot conduct secondary acquisitions on their own behalf.

Where secondary acquisitions are undertaken through an ESOP trust, the prescribed limits apply to the trust.

- Annual cap: no more than two percent of paid-up equity capital per financial year.

- Aggregate cap: no more than five percent of paid-up equity capital at any point in time, for ESOS, ESPS, and SAR schemes combined.

These caps do not apply to new shares issued by the company to the trust, or to shares gifted by promoters or shareholders. If option grants exceed what secondary acquisition can cover, the shortfall must be met by fresh share issuance to the trust.

For a detailed explanation of how ESOP trusts are structured and funded, see ESOP Trust in India: Why Public Companies Use Them.

Approvals required before launching a scheme

No scheme can be offered until shareholders approve it by special resolution, meaning votes cast in favour must be not less than three times the votes cast against, passed in a general meeting.

Beyond the initial scheme approval, separate resolutions are required for: secondary acquisition of shares by the trust; grants to employees of subsidiary or holding companies; and grants to any individual equal to or exceeding one percent of issued capital in one year.

Every listed company implementing a scheme must also constitute a compensation committee to administer it. The committee formulates detailed terms and conditions, determines grant eligibility, and frames policies to prevent insider trading violations by the trust, the company, and its employees.

Key scheme terms: vesting periods, exercise pricing, and separation rules

Vesting

Both ESOS and SAR schemes require a minimum vesting period of one year from the date of grant. Companies may set longer periods or tie vesting to performance milestones.

Two exceptions apply:

- If an employee dies or becomes permanently incapacitated while in employment, all granted options shall vest immediately on that date. In both cases, the minimum one-year vesting period is waived.

- Retirement or superannuation is treated differently from resignation. On retirement, unvested grants do not automatically lapse; the scheme terms, as determined by the compensation committee, govern whether vesting continues on the original schedule or is otherwise managed.

Pricing

For ESOS, companies are free to set the exercise price at any level, subject to complying with applicable accounting standards under Regulation 15, including Ind AS 102 for companies following Indian Accounting Standards. The resulting compensation cost must be correctly recognised and disclosed.

For sweat equity, pricing is not discretionary: it must follow the preferential issue pricing requirements under the SEBI ICDR Regulations, 2018.

Separation events

Separation events are circumstances that change or end an employee's relationship with the company. The SBEB Regulations prescribe certain mandatory rules and permit scheme-specific treatment for different separation events.

- Resignation or termination: Unvested grants lapse on the date of separation. Vested grants are retained by the employee, subject to the terms and conditions the compensation committee has set under the scheme.

- Death: All grants, whether vested or unvested, vest immediately on the date of death in the legal heirs or nominees of the deceased employee.

- Permanent incapacity: All grants vest immediately on the date of permanent incapacitation, regardless of the original vesting schedule.

- Retirement or superannuation: Unvested grants do not lapse. They continue to vest in accordance with the original vesting schedule after retirement, subject to the company's applicable policies and law.

- Transfer or deputation to an associate company: Vesting and exercise continue under the original terms of the grant, even after the transfer or deputation takes effect.

All grants, regardless of the separation event, are non-transferable and cannot be pledged, hypothecated, or mortgaged at any point.

Disclosure requirements for listed companies

The SBEB Regulations prescribe disclosure obligations across three channels: the Board of directors report and company website, stock exchange filings, and the secretarial auditor certificate at the AGM.

Board of directors report and company website

The board must confirm in its report whether the scheme is in compliance with the regulations and disclose any material change to the scheme during the year. The company's website must carry the following details, with a web link provided in the board report:

- Option movement during the year: number of options granted, vested, exercised, lapsed, and outstanding

- Weighted-average exercise prices and weighted-average fair values, disclosed separately for options whose exercise price equals, exceeds, or is less than the market price

- Employee-wise details for senior managerial personnel, any employee receiving five percent or more of total options granted during the year, and any employee receiving grants equal to or exceeding one percent of issued capital in a single year

- Diluted earnings per share on shares issued pursuant to all schemes, in accordance with applicable accounting standards

Equivalent disclosures apply for SAR schemes and ESPS allotments made during the year.

Stock exchange filings

Before making any grant, the company must file scheme details with the recognised stock exchange in the format prescribed in Part D of Schedule I of the SEBI (Share Based Employee Benefits and Sweat Equity) Regulations, 2021 and obtain in-principle approval. After each exercise, the stock exchange must be notified in the format specified in Part E of Schedule I.

Secretarial auditor certificate

At every Annual General Meeting, the board must place before shareholders a certificate from the secretarial auditor confirming that the scheme has been implemented in accordance with the regulations and with the resolutions passed by shareholders.

Disclosure obligations under SEBI (LODR) Regulations

Beyond the SBEB Regulations, listed companies must also comply with the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (“LODR”). Regulation 30 of the LODR Regulations, read with Schedule III, identifies three situations in which listed companies must make stock exchange disclosures relating to share-based employee benefit schemes.

- First, when the board of directors approves a proposal to establish or amend an ESOP scheme, including a decision to seek shareholder approval, the outcome of that board meeting must be disclosed to the stock exchange.

- Second, once shareholders approve the scheme at a general meeting, the proceedings of that meeting must be disclosed to the stock exchange.

- Third, certain events relating to ESOP or ESPS schemes may require disclosure to the stock exchange if they are considered material under Regulation 30 of the SEBI (LODR) Regulations. Unlike Para A events, which are deemed material automatically, Para B events require the board to apply the materiality criteria under Regulation 30(4). These criteria include whether omission of the information is likely to result in a significant market reaction, or whether the value or expected impact of the event exceeds the prescribed quantitative thresholds. If the board determines that an event relating to the scheme is material under these criteria, disclosure to the stock exchange is required.

Companies should ensure that these LODR filings are coordinated with the in-principle approval and post-exercise notification processes under Regulation 10 of the SBEB Regulations. The two frameworks operate in parallel, and compliance with one does not satisfy the obligations under the other.

Quantitative caps on sweat equity issuance

Sweat equity issued by a listed company under Chapter IV is subject to the following quantitative caps under Regulation 31:

- No more than fifteen percent of existing paid-up equity share capital may be issued as sweat equity in any financial year.

- The aggregate sweat equity issued must not exceed twenty-five percent of paid-up equity share capital at any time.

Exception: companies listed on the Innovators Growth Platform (IGP), a SEBI-regulated board for emerging and startup-stage companies, may issue up to fifty percent in aggregate within ten years of incorporation.

Each issuance requires a separate special resolution valid for twelve months. Where sweat equity is issued to promoters or the promoter group, a resolution passed by simple majority (>50%) is required in a general meeting, and the promoters themselves cannot vote on that resolution.

How the 2025 amendments changed the regulations

Two amendments to the SBEB Regulations came into force in 2025.

Regulation 9A: Employee identified as a promoter or a part of promoter group in the draft offer document

When an employee (or a founder) who holds ESOP grants is later identified as a promoter or promoter group member in the Draft Red Herring Prospectus (DRHP), the preliminary offer document filed with SEBI as part of the IPO process), the original regulations would have caused those grants to lapse because promoters are excluded from scheme eligibility.

Regulation 9A resolves this: an employee identified as a promoter or promoter group member in the DRHP, whose options, SARs, or other benefits were granted at least one year before the IPO filing, may continue to hold and exercise those grants on their original terms.

Valuer definition

In SEBI (Share Based Employee Benefits and Sweat Equity) (Second Amendment) Regulations, 2025, the definition of "valuer" in Regulation 2(1)(ww) was updated to align with Section 247 of the Companies Act, 2013. Previously, the valuer responsible for sweat equity valuations was defined as an independent chartered accountant or merchant banker. The amendment replaces this with a registered valuer, meaning a professional registered with the Insolvency and Bankruptcy Board of India (IBBI).

Regulation 34(1) now requires all new valuations to be conducted only by registered valuers. Merchant bankers who had already taken up valuation assignments before the amendment came into force may complete those assignments within nine months of the effective date.

Tax treatment for employees

ESOP exercise at a listed company triggers a perquisite tax on the spread between the fair market value of the shares on the exercise date and the exercise price, which the employer must deduct as TDS. On subsequent sale, capital gains tax applies on any further appreciation above the fair market value at exercise.

For a detailed analysis of ESOP taxation at listed and unlisted companies, see the EquityList guide to ESOP taxation in India.

FAQs on SEBI ESOP regulations

Do SEBI ESOP regulations apply to all companies?

No. The SEBI (Share Based Employee Benefits and Sweat Equity) Regulations, 2021 apply only to companies whose equity shares are listed on a recognised stock exchange in India. Unlisted companies are governed instead by Section 62(1)(b) of the Companies Act, 2013 read with the Rule 12 of Companies (Share Capital and Debentures) Rules, 2014, which prescribe a separate and less detailed framework. If an unlisted company is preparing for an IPO and has a pre-IPO scheme in place, that scheme must be brought into conformity with the SBEB Regulations and ratified by shareholders after listing before any fresh grants can be made under it.

Which employees are eligible for ESOPs under SEBI regulations?

Employees eligible under Regulation 2(1)(i) include employees designated by the company working in India or abroad, whole-time and non-executive directors (excluding independent directors), and employees or directors of group companies, subsidiaries, associate companies, and holding companies. Promoters, promoter group members, independent directors, and directors holding more than ten percent of the company's outstanding equity shares (directly or indirectly) are explicitly excluded. Non-permanent and contractual employees working exclusively for the company became eligible under the 2021 regulations, which removed the word "permanent" from the earlier definition.

What is the minimum vesting period under SEBI ESOP regulations?

The minimum vesting period for ESOS and SAR schemes is one year from the date of grant, per the SBEB Regulations, 2021. Companies may set longer periods or structure vesting around performance milestones. Two exceptions apply: death or permanent incapacity of an employee in service triggers immediate vesting of all granted options, regardless of the original schedule.

Can promoters hold ESOPs in a listed company?

Promoters and promoter group members are excluded from eligibility under the SBEB Regulations. The September 2025 amendment (Regulation 9A) creates a limited exception: a founder who received ESOP grants as an employee, and is subsequently identified as a promoter in the DRHP at least one year after those grants were made, may retain and exercise those pre-existing grants on their original terms.

.png)