.avif)

TL;DR

Underwater options happen when your employee stock options have a strike price higher than your company's current fair market value. This makes them worthless as incentives. The usual cause is a down-round. You have three main fixes: repricing (you adjust the strike price), option exchange programs (you swap old options for new ones), or alternative compensation (you give RSUs or cash bonuses). Each fix has different tax and accounting impacts in the US and India. Sometimes doing nothing is your best move if you expect the stock price to recover quickly.

When employee stock options go underwater, they stop motivating your team. They start driving people away instead. Here's how you can fix underwater options before you lose your best people.

What does "underwater options" mean?

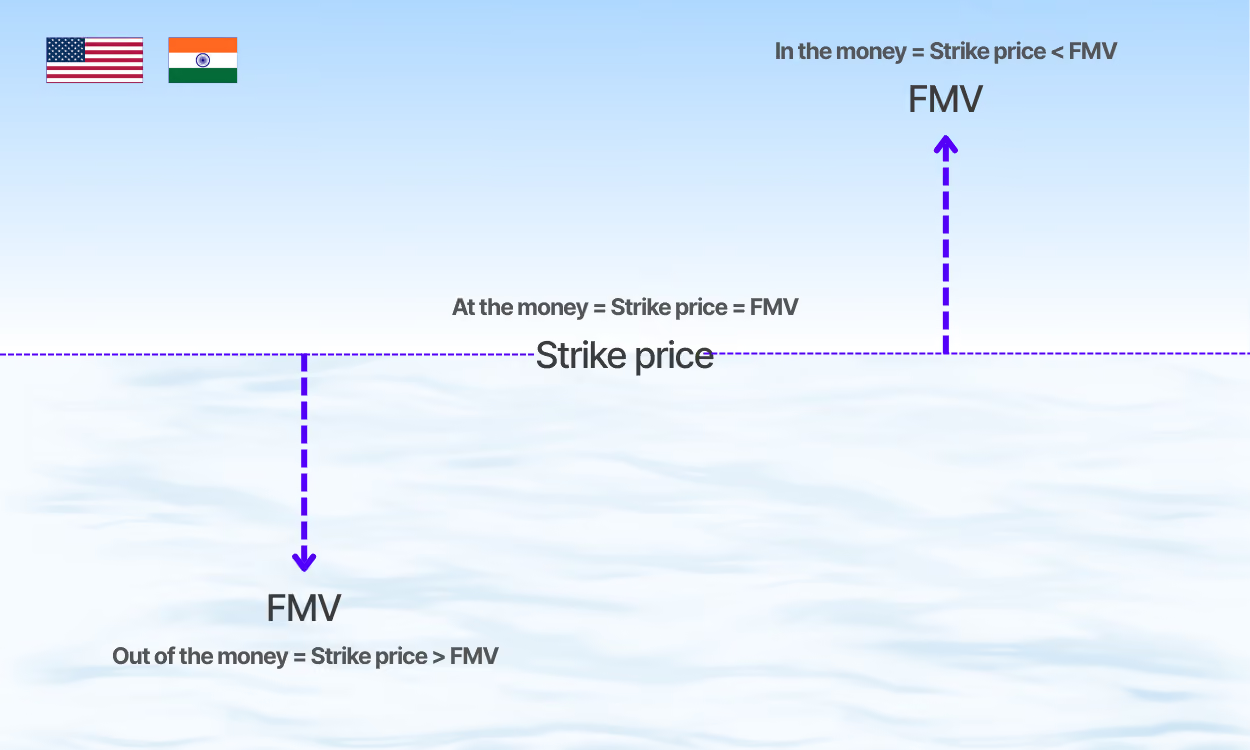

An option is underwater (also called "out-of-the-money") when its exercise price is higher than the stock's current Fair Market Value (FMV).

Simple example: Your employee has options with a $10 strike price. Your company's current FMV is $6. They would pay $10 to buy something worth $6. That's a guaranteed $4 loss per share. No rational employee exercises underwater options.

This is the problem: underwater stock options have zero incentive value. You designed equity compensation to retain and motivate your team. It becomes meaningless overnight.

What makes stock options go underwater?

A down-round causes most underwater employee stock options. This is a financing event where your startup raises capital at a valuation lower than the previous round.

Here's how it happens:

Scenario:

- Series A valuation: $50 million (FMV: $10 per share)

- You grant options to employees at $10 strike price

- Series B valuation: $30 million (FMV: $6 per share)

- All options granted at $10 are now underwater

The valuation drops. The FMV drops with it. You granted the original stock options at the old, higher price. They instantly lose their value. The dilution from the new funding round makes the problem worse.

Real-world context: When this happens

Underwater options typically occur during:

- Market corrections or economic downturns

- Competitive pressure that forces lower valuations

- Missed growth targets that lead to down-rounds

- Pivot scenarios that require bridge financing at reduced valuations

We saw this frequently in 2022-2023 in both India and the US. Valuations corrected from 2021 highs. Indian startups with $1B+ valuations saw down-rounds of 30-50%. This instantly created underwater stock option problems across entire organizations.

The real cost: Morale, retention, and hiring

Underwater options create three critical business problems.

1. Retention risk

Your employees see their options as worthless. Your best talent can get in-the-money equity elsewhere. They will leave. Your underwater options become a competitive disadvantage against companies offering valuable equity.

2. Trust erosion

When equity compensation becomes worthless, it erodes faith in your company's long-term value. Employees feel betrayed by the promise of wealth-building through ownership.

3. Hiring handicap

New candidates demand higher cash salaries. Your equity package no longer offsets lower base pay. This damages your total compensation competitiveness. It burns more runway.

The math: You typically offer a $100K salary + $50K in equity value. Your equity is underwater and worthless. You now need to pay $150K in cash to compete. That's a 50% increase in your cash burn.

3 strategies to fix underwater options

You have three main approaches to repair underwater stock options. Each has different tax implications and accounting costs. This is particularly true between the US and India.

1. Option repricing (the simple fix)

What it is: You amend the existing option agreement. You reduce the strike price to match the current FMV.

How it works:

- Original grant: 10,000 options at $10 strike price (FMV was $10)

- Current situation: FMV is now $6, options are $4 underwater

- Repricing solution: You amend strike price to $6

- Result: Options are now at-the-money with upside potential

a. Legal requirements

US compliance:

- Set the new exercise price at or above the current FMV

- Get a current 409A valuation to establish FMV

- Follow your equity plan's repricing provisions

- Get shareholders to approve (often required)

India compliance:

- Set the new strike price at or above FMV (determined by merchant banker valuation or per SEBI guidelines)

- Get board to approve and typically shareholders to approve

- Comply with Companies Act 2013 requirements

b. Tax implications

US tax risks:

For Incentive Stock Options (ISOs):

- We treat repricing as a cancellation plus new grant

- This restarts the 2-year holding period for favorable tax treatment

- It can accidentally convert ISOs to Non-Qualified Stock Options (NSOs) if you don't structure it carefully

- NSOs result in ordinary income tax (up to 37% federal) vs. long-term capital gains (20%)

Example tax impact:

- Employee exercises 10,000 repriced options

- If NSO: Ordinary income tax on spread ($40K at 37% = $14,800)

- If ISO (maintained): No immediate tax, potential LTCG at sale (20%)

- Difference: $14,800+ in immediate tax liability

For NSOs: This is less problematic. But it still resets vesting schedules if you implement new vesting.

India tax treatment:

- Repricing itself doesn't trigger immediate taxation

- Tax hits at exercise (perquisite tax on spread between FMV and strike price)

- For listed companies: Securities Transaction Tax (STT) applies on transactions of listed securities, not specifically to ESOP taxation at exercise. The perquisite tax applies regardless

- Income tax rates: Up to 30% plus surcharge and cess

c. When to use repricing

Use this for:

- Small teams (< 50 employees) where you can manage individual treatment

- Private companies with flexible governance

- When you want to maintain original grant sizes

- Situations where you can accept accounting complexity

Accounting impact: Under ASC 718 (US) or Ind AS 102 (India), repricing creates incremental compensation expenses. This equals the increase in fair value of the modified award. This hits your P&L immediately.

2. Option exchange program (the modern fix)

What it is: Your employees voluntarily exchange underwater stock options for new options at the current lower FMV. The most common method is a value-for-value exchange.

a. How to calculate fair value

You don't do a 1-for-1 exchange. You use the fair value of the old underwater options. This determines how many new at-the-money options you grant.

Detailed example:

Starting position:

- Employee has: 10,000 options at $10 strike price

- Current FMV: $6 per share

- Options are $4 underwater

Calculate the fair value:

- Old options fair value: $2 per option (using Black-Scholes or similar)

- Total value of old grant: 10,000 × $2 = $20,000

- New at-the-money options fair value: $4 per option

- New options to grant: $20,000 ÷ $4 = 5,000 options

Result: Employee exchanges 10,000 underwater options for 5,000 at-the-money options at $6 strike price.

b. Why investors prefer this

Value-for-value exchanges reduce dilution:

- Old underwater grant: 10,000 options (0.10% of company)

- New at-the-money grant: 5,000 options (0.05% of company)

- You reduce dilution by 50% while restoring incentive value

This protects preference share holders and other investors from excessive dilution. You still solve the retention problem.

c. Program requirements

US requirements:

- Make participation voluntary (you can't force it)

- Get shareholders to approve for public companies (typically required)

- Follow SEC Rule 13e-4 for tender offer rules if applicable

- Get an updated 409A valuation

India requirements:

- Get board and shareholders to approve

- Follow SEBI ESOP guidelines for listed companies

- Get valuation by merchant banker for price determination

- File RBI reporting if you involve foreign shareholders

d. Tax treatment

US:

- The exchange itself is generally not a taxable event

- You face no immediate tax consequences

- We tax new options normally at future exercise

India:

- The exchange itself is not a taxable event

- Future taxation on exercise and sale follows standard ESOP rules

e. When to use exchange programs

Use this for:

- Medium to large teams (50+ employees)

- Companies with active investor oversight

- When you need to manage overall dilution carefully

- Situations where you want to reset vesting schedules

3. Cash-outs or alternative grants (the certainty fix)

If option repricing or exchanges are too complex, use alternative compensation. This restores incentive value.

a. Three alternative approaches

i. Restricted Stock Units (RSUs)

Grant RSUs instead of options:

- How it works: You promise shares outright upon vesting. There's no strike price to pay.

- Value: More certain. RSUs always have value unless shares become worthless.

- Downside: We tax them as ordinary income on vesting

Example:

- Cancel 10,000 underwater options at $10 strike

- Grant 3,000 RSUs at $6 FMV

- Employee receives $18,000 in stock value over time (no need to buy)

US tax: Ordinary income on $18K when RSUs vest (up to 37% federal rate) India tax: Taxed as perquisite on vesting (up to 30% + surcharge)

ii. Cash retention bonuses

Pay immediate cash bonuses with clawback provisions:

- How it works: You give cash equal to lost option value. You require repayment if the employee leaves within X months.

- Value: Immediate liquidity. This solves the morale problem now.

- Downside: Uses precious cash. Triggers ordinary income tax.

Example:

- Underwater loss: 10,000 options × $4 underwater = $40K lost value

- Grant: $20K retention bonus (50% of loss)

- Terms: Must stay 18 months or repay

iii. Performance bonuses tied to milestones

Structure cash bonuses tied to company recovery:

- Pay bonuses if company hits valuation milestones

- This aligns incentives with company recovery

- You preserve cash until success

b. When to use alternative compensation

Use this for:

- Quick fixes without complex restructuring

- Small number of key employees

- When legal/accounting costs outweigh benefits of formal repricing

- Bridge solution while you plan full option exchange

The dilution dilemma: Getting shareholder approval and managing overhang

Any underwater options fix that restores employee equity value reduces your investors' share in future profits. This is the dilution dilemma you must navigate.

1. Understanding option overhang

Option overhang = (Outstanding options + Available pool) ÷ Fully diluted shares

Calculate it like this:

- Total shares outstanding: 10,000,000

- Outstanding options: 1,500,000

- Available option pool: 500,000

- Overhang: 2,000,000 ÷ 10,000,000 = 20%

Repricing or granting new options increases overhang. Preference shareholders watch this number carefully. It directly impacts their returns at exit.

2. How to get shareholder approval

For US companies:

- Public companies: NYSE/NASDAQ require shareholder vote for repricing

- Private companies: Depends on charter and investor rights

- Preferred shareholders often have protective provisions

For Indian companies:

- Board approval: Required for any ESOP amendment

- Shareholder special resolution: Required for material modifications

- Notification to stock exchanges (if listed)

3. Making the business case to investors

Prepare a data-driven proposal.

a. Retention risk analysis:

- Calculate replacement cost for key employees

- Show market rates for equivalent talent

- Highlight critical personnel flight risk

Example pitch: "Our CTO and 3 senior engineers have a combined salary of $800K/year. They have 100% underwater options. Replacement cost: $200K recruiting fees + 6 months hiring time + 12 months ramp-up. Total risk: $1.2M+ vs. $150K dilution cost from repricing."

b. Value-for-value proposal: Show reduced dilution through exchange ratios:

- Old program: 2,000,000 options underwater

- Value-for-value exchange: 1,000,000 new options at-the-money

- Net dilution reduction: 1,000,000 shares (10%)

c. Waterfall modeling: Use cap table scenario analysis to show minimal impact on investor returns:

- Model exit at $100M, $150M, $200M valuations

- Show investor returns with and without repricing

- Demonstrate that talent retention increases exit probability

The key argument: The cost of losing key talent is far higher than the dilution cost of a controlled equity fix.

The "wait-and-see" strategy: When doing nothing is best

Not every underwater option situation requires immediate action. A formal repricing is expensive. It signals financial trouble to employees and the market. Sometimes patience is your optimal strategy.

1. When to wait rather than reprice

Choose the wait-and-see strategy if:

a. The market dip is temporary (12-18 month recovery expected)

Wait if you have strong conviction about near-term recovery:

- The recent down-round was market-driven, not performance-driven

- Your fundamentals remain strong (revenue growth, customer retention)

- Industry sentiment is improving

- The bridge round was opportunistic, not desperate

Example: Your SaaS company raised at $30M down from $50M in Q4 2022. But ARR is growing 100% YoY. Your metrics suggest Series B at $70M+ in 2024. Options at $10 strike with $6 FMV may be valuable again in 18 months.

b. Options are only slightly underwater

Small amounts underwater (< 20%) often recover naturally:

- Strike price: $10

- Current FMV: $8.50

- 15% underwater — likely to recover with normal growth

vs.

- Strike price: $10

- Current FMV: $4

- 60% underwater — requires intervention

c. Legal and accounting costs are prohibitive

Full repricing costs for a 100-person company:

- Legal fees: $25,000-$50,000

- 409A valuation: $10,000-$20,000

- Accounting expense (ASC 718): $200,000-$500,000 one-time charge

- Total cost: $235,000-$570,000

If you only have $500K runway remaining, you can't justify these costs.

2. Interim solutions while waiting

If you choose to wait, take these steps:

a. Transparent communication:

- Explain the down-round honestly

- Show the business recovery plan

- Give realistic timeline for FMV recovery

- Hold quarterly updates on progress

b. Partial cash compensation:

- Give small retention bonuses for critical employees

- Pay quarterly performance bonuses to bridge the gap

- Offer non-equity perks (flexibility, learning budgets, etc.)

c. Selective repricing:

- Reprice only for top 10-15 critical employees

- Minimize costs while managing highest flight risk

- Plan full program once finances improve

The founder's communication playbook

Technical execution matters. But communication determines whether your underwater options fix succeeds or fails. Your employees need to understand what happened, why it matters, and what you're doing about it.

Step 1: Own the situation (don't make excuses)

Bad approach: "Due to market conditions beyond our control, we experienced a down-round that unfortunately impacted option values. We're exploring solutions."

Good approach: "We raised at a lower valuation. This made your options worthless. That's unacceptable. Here's what happened, what we're doing to fix it, and what it means for you."

Frame the repricing as an investment in your team's future. Don't position it as damage control for past mistakes.

Step 2: Explain the mechanics simply

Most employees don't understand options deeply. Use concrete examples like:

Step 3: Focus on future upside

The repricing restores potential. It doesn't fix the past. Emphasize forward-looking value:

"Your new $6 strike price means this: If we execute our plan and exit at $20 per share, you make $14 per share profit. That's $140,000 on your 10,000 options. The old $10 strike price would give you $10 per share profit—$100,000. The repricing gives you 40% more upside."

Step 4: Hold dedicated Q&A sessions

Run small-group sessions with your legal and finance teams:

- Address tax questions individually

- Provide written summaries employees can reference

- Create a single FAQ document as the source of truth

- Offer one-on-one sessions for senior employees with complex situations

Step 5: Give regular updates on progress

After repricing, update quarterly on company performance:

- Share key metrics showing recovery

- Show FMV progression (if possible)

- Celebrate milestones that increase option value

- Remind people of their upside potential

US vs India: Key regulatory differences

The economic principles of underwater options are universal. But legal and tax treatment differs significantly between jurisdictions.

1. Valuation requirements

US:

- 409A valuation required for strike price setting

- Update it at repricing

- We recommend independent valuation firm

- Valid for 12 months or until material event

India:

- Merchant banker valuation for listed companies

- Private companies: Can use discounted cash flow or comparable company analysis

- SEBI guidelines specify methodologies

- More flexibility in valuation approach

2. What approvals you need

US:

- Board must approve for private companies (unless charter restricts)

- Public companies: Shareholders must approve repricing

- Depends on equity plan provisions

India:

- Board must always approve

- Shareholders must pass special resolution for ESOP amendments

- Listed companies: File extra SEBI disclosures

3. Tax treatment summary

US:

- ISO repricing = new grant (restarts holding period)

- NSO repricing = less complicated

- AMT implications on ISO exercise

- Capital gains treatment requires 2-year hold from grant + 1-year from exercise

India:

- Perquisite tax at exercise (difference between FMV and strike price)

- Tax rate: Up to 30% + surcharge + 4% cess = ~35% effective (the actual number depends on your income slab)

- LTCG tax at sale: 12.5% on LTCG for listed shares (above ₹1.25 lakh exemption), 12.5% for unlisted shares without indexation

- No AMT considerations

4. Accounting standards

US: ASC 718

- Repricing creates incremental compensation expense

- Expense = increase in fair value from modification

- Hits P&L over remaining service period

India: Ind AS 102

- Similar to ASC 718 conceptually

- Modification accounting required

- Must recognize incremental fair value

FAQs

1. What does it mean if options are underwater?

Options are underwater (or "out-of-the-money") when the exercise price is higher than the current fair market value (FMV) of the company stock. Underwater stock options have zero intrinsic value. No one will pay more to buy a share than its current worth. For example, options with a $10 strike price when the FMV is $6 are $4 per share underwater.

2. What to do if stock options are underwater?

As a founder, you have three primary strategies to fix underwater options:

- Option repricing: Reduce the strike price to match current FMV

- Option exchange program: Swap underwater options for at-the-money options (value-for-value)

- Alternative compensation: Grant RSUs, cash bonuses, or performance-based payments

The right choice depends on your company size, investor relationships, and how severe the underwater situation is. For slightly underwater options with expected near-term recovery, waiting may be your best strategy.

3. What are underwater stocks?

"Underwater" technically applies to options, not stocks. If someone bought shares directly and the market price dropped below their purchase price, we use different terms. The correct terms are "holding at a loss" or "negative equity position." We use the underwater terminology specifically for options and derivatives—where you compare strike price to market price.

4. What is the $100,000 rule for stock options?

The $100,000 rule is a US tax regulation for Incentive Stock Options (ISOs). It limits the aggregate fair market value of ISOs that can first become exercisable in any calendar year to $100,000. We measure this at the grant date FMV. Any ISOs exceeding this limit are automatically treated as Non-Qualified Stock Options (NSOs). NSOs have less favorable tax treatment.

Example: You grant an employee ISOs on 20,000 shares at $10 FMV with 4-year monthly vesting. Each year, 5,000 shares vest = $50,000 value. This stays under the limit. But if you are granted 1-year cliff vesting and all 20,000 shares become exercisable in year one. That’s $200,000 in value. Under the rule, the first $100,000 can be ISOs, and the remaining $100,000 must be treated as NSOs.

5. Do you get a tax loss when you exercise underwater options?

No. Never exercise underwater stock options. This means paying more than the current value—a guaranteed loss. If you did exercise underwater options, you wouldn't recognize a tax loss. This happens only when you eventually sell the shares for less than your total cost basis (strike price paid + any taxes). The IRS doesn't let you claim a loss on the exercise itself.

6. Do I lose my stock options if I get fired?

In almost all cases, yes. You lose unvested options immediately upon termination. For vested options, you typically have a short window to exercise them before they expire. This is usually 30 to 90 days (called the Post-Termination Exercise Period or PTEP). This is true whether you resign, your company fires you, or you leave for any reason other than death or disability. Those may have different terms.

Some progressive companies now offer extended post-termination exercise periods of up to 10 years. But this is still rare.

7. Should I exercise stock options immediately?

No, not if they're underwater. Exercising underwater options means paying cash for a guaranteed loss. Early exercise makes sense only for deep early-stage grants where:

- FMV is still very low (pennies per share)

- You want to start the capital gains holding period clock

- Options are at-the-money or in-the-money

- You can afford the tax consequences

- You believe strongly in long-term upside

For underwater employee stock options, wait until the FMV rises above your strike price. Only then does exercising make sense.

8. What does the term underwater mean in finance?

In finance, "underwater" generally means an asset is worth less than its cost or associated debt. The term applies to:

- Options: Strike price exceeds current market value

- Real estate: Mortgage balance exceeds property value

- Investments: Current value is below purchase price

The term comes from the metaphor of submersion. You're below the surface (breakeven point) rather than above it (profitable).

9. What is an underwater valuation?

"Underwater valuation" isn't a standard finance term. "Underwater" describes an option's status relative to current value. The event that causes options to go underwater is called a down-round. This is when your company raises capital at a valuation lower than the previous financing round. The down-round lowers the FMV. This makes previously granted options underwater.

Need help managing your equity compensation through challenging times? EquityList provides cap table management, ESOP administration, and scenario modeling for startups in India and globally.

.png)