Modeling different funding scenarios isn’t just a “nice to have”; it’s one of the most important parts of founder decision-making. Every round of financing changes ownership, control, dilution, and the value of each share. A cap table that supports scenario modeling helps you predict these outcomes before committing to a raise, letting you make decisions with clarity.

In this guide, we break down exactly how to simulate multiple funding scenarios in a cap table and which tools founders, CFOs, and investors rely on to do it.

Steps for simulating multiple funding scenarios in a cap table

1. Start with a clean baseline

Begin by setting up your current ownership structure. This becomes the foundation for every scenario you create.

Include:

- Founders’ shares

- Employee option pool (both granted and unallocated)

- Existing SAFEs or convertible notes

- Previous investors or past financing rounds

Your baseline should reflect the exact number of fully diluted shares. This includes:

- All issued shares

- All granted options

- All unissued options

- All SAFEs and notes converted as if a round happened today

Modeling with fully diluted shares provides an accurate view of total potential equity and prevents underestimating dilution.

2. Define your fundraising round assumptions

Each scenario depends on the specific inputs or assumptions you choose to model.

These inputs describe the terms of the round you are simulating, and even small changes can meaningfully shift ownership outcomes.

For each scenario, outline:

- Pre-money valuation

- Amount of new capital raised

- ESOP pool expansion, if required by investors

- Instrument type, such as a SAFE, priced round, convertible note, or a combination

These assumptions help you see how small changes in valuation, dilution terms, or round size affect ownership.

3. Build multiple scenarios

Once your assumptions are ready, create several versions of how the company might raise money. This lets you compare outcomes side by side.

Examples:

- Scenario A: Raise $1.5M SAFE at a $6M cap

- Scenario B: Raise $2M priced round at an $8M pre-money

- Scenario C: Raise $1M SAFE now and a $1M priced round later

- Scenario D: Raise capital with an ESOP expansion versus raising without increasing the pool

The goal is to understand how different fundraising paths change dilution and long-term ownership.

4. Apply conversion rules

Next, model how each instrument converts into shares.

Convert each instrument based on:

- The discount rate

- The valuation cap

- Accrued interest, in the case of notes

- The round share price (the discount applies relative to this price)

Accurate conversion is essential because SAFEs and notes almost never convert at the same price as new investors. Their caps and discounts give them more shares for the same investment amount, which increases dilution for founders and early shareholders.

5. Add option pool changes

Sometimes new investors in a priced round require increasing the ESOP pool to ensure enough equity is available for future hiring.

These pool expansions almost always happen before the new investor comes in, which means the dilution falls mostly on founders and early shareholders. It’s one of the most common sources of unexpected dilution, so it should always be modeled explicitly.

6. Compare outcomes

With all assumptions and conversions applied, your cap table should now show the final fully diluted structure for each scenario.

You should be able to compare:

- New ownership percentages

- Post-money valuation

- Dilution for each stakeholder

- Share price for each scenario

This comparison helps you understand which fundraising path leads to the healthiest long-term cap table and which one creates unnecessary dilution.

Modeling funding scenarios in a cap table

Now that the mechanics of scenario modeling are clear, this section shows how the numbers actually play out.

Base cap table

Assume the company currently has:

- 1,000,000 founder shares

- 200,000 options (unallocated)

- No SAFEs or notes

- No previous investors

Total fully diluted shares: 1,200,000

This will be our reference point across scenarios.

Ownership before any fundraising

Scenario 1: SAFE investment followed by a Seed round

Step 1: SAFE conversion

The company raises a $1M SAFE at a $5M cap, then raises a Seed round at a $7M pre-money valuation with a $2M investment.

During the priced round, the SAFE converts at its $5M cap because it is lower than the round valuation. If the round valuation were below the cap, the SAFE would instead convert at the round price.

Conversion price

= $5,000,000 cap ÷ 1,200,000 shares

= $4.17 per share

SAFE shares issued

= $1,000,000 ÷ 4.17

≈ 239,808 shares

Step 2: Seed round

Seed share price

= $7,000,000 ÷ (1,200,000 + 239,808)

≈ $4.9 per share

Seed shares issued

= $2,000,000 ÷ 4.9

≈ 408,163 shares

Scenario 2: Multiple SAFEs with different terms

Assume the company raises two SAFEs before the Seed round:

- SAFE A: $500k investment at a $4M cap

- SAFE B: $500k investment at a $6M cap

Step 1: SAFE conversion

SAFE A share price

= $4,000,000 ÷ 1,200,000 shares

= $3.33 per share

Shares issued

= 500,000 ÷ 3.33

≈ 150,150 shares

SAFE B share price

= $6,000,000 ÷ 1,200,000 shares

= $5 per share

Shares issued

= 500,000 ÷ 5

= 100,000 shares

Step 2: Seed round at $7M pre-money with $2M invested

Total shares after SAFEs: 1,450,150

Seed share price

= $7,000,000 ÷ 1,450,150

≈ $4.83 per share

Seed shares issued

= $2,000,000 ÷ 4.83

≈ 414,078 shares

Earlier, pre-money SAFEs were more common in the ecosystem. In that structure, all SAFEs convert together before the priced round, which means they dilute the founders and also dilute one another, making pre-money SAFEs generally more founder-friendly. Today, companies more often use post-money SAFEs, where each investor’s ownership is fixed in advance. As a result, SAFEs no longer dilute each other; instead, the full dilution falls on the founders and existing shareholders, as shown in our example.

Scenario 3: Option pool expansion with a convertible note and a Seed round

The company previously raised a $500k convertible note on the following terms:

- Valuation cap: $6M

- Discount: 20%

- Interest: ignored for simplicity

Step 1: Note conversion price

The note tests two prices; the lower applies:

- Cap-based price: $6,000,000 ÷ 1,200,000 shares = $5 per share

- Discount-based price: Round share price × (1 − discount). This is calculated after the price per share for the priced round is known.

To simplify modeling, we proceed using the cap price.

Note amount ÷ conversion price

= $500,000 ÷ 5

= 100,000 new shares

Updated shares before pool expansion:

1,200,000 + 100,000 = 1,300,000

Step 2: Investor requires an option pool expansion before the round

The company has an existing pool of 200,000 options, but the new investor wants the pool expanded before the round so that it represents 15% of the cap table on a pre-money basis. Since the expansion happens before the round, the dilution falls entirely on the founders and existing shareholders.

Let X = new pool size (after expansion).

X = 15% of total shares post-expansion.

Equation:

X = 0.15 × (1,300,000 + X)

Solve:

X = 195,000 + 0.15X

0.85X = 195,000

X ≈ 229,411 shares

Existing pool = 200,000

New pool shares added = 29,411

Total shares before priced round:

1,300,000 + 29,411 = 1,329,411

Step 3: Priced round

The company raises $2M at an $8M pre-money valuation.

Round share price:

$8,000,000 ÷ 1,329,411

≈ $6.02 per share

Shares issued to the Seed investor:

$2,000,000 ÷ 6.02

≈ 332,225 shares

Scenario 4: $50M exit

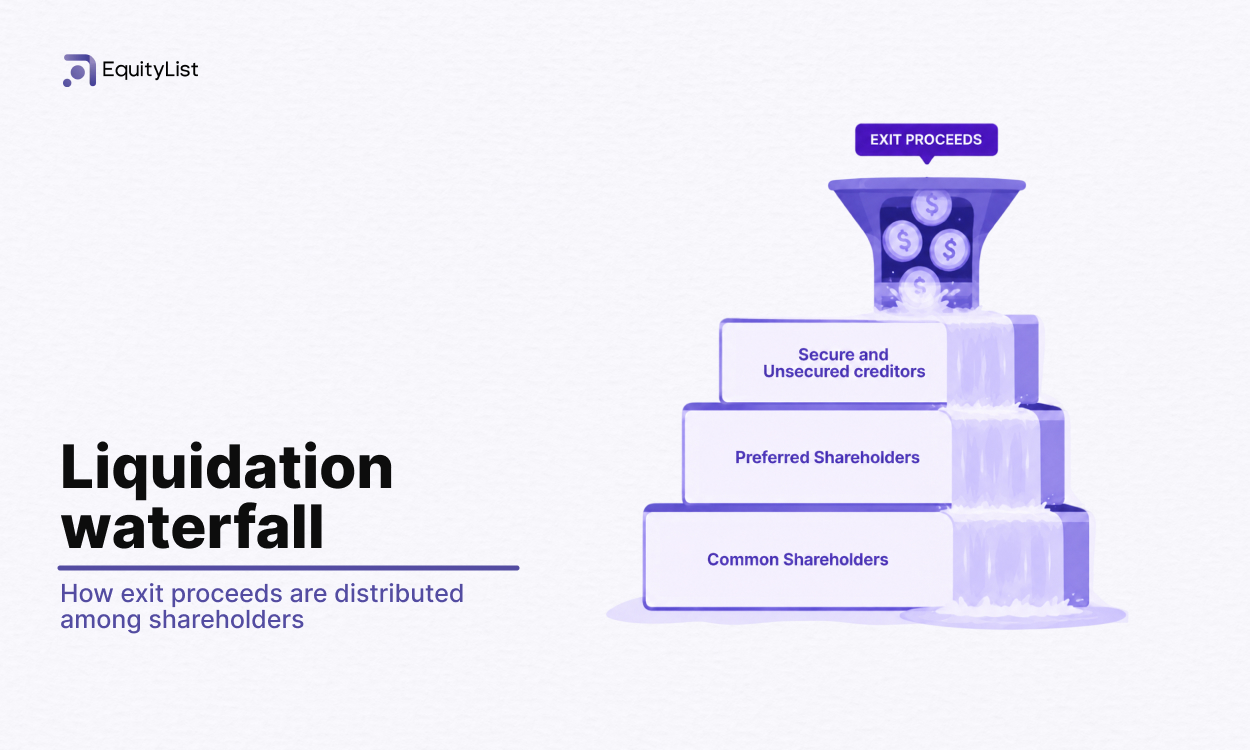

Before distributing proceeds, all SAFEs and notes convert so ownership is correctly reflected. Exit modeling follows a strict order because each security type has specific payout rights.

Using Scenario 2’s structure:

Step 1: Convert SAFEs into shares

SAFE A and SAFE B convert at their caps. Safe holders now participate as shareholders.

Step 2: Apply liquidation preference

Investors who participated in priced rounds typically hold preferred shares, which entitle them to receive their original investment amount (or a multiple, depending on the terms) before common shareholders receive proceeds. In Scenario 2, the Seed investor has a 1x non-participating preference, so they receive their $2M investment first.

Remaining proceeds:

$50M − $2M = $48M

After preferences are satisfied, the remaining exit value is shared proportionally according to each stakeholder’s final fully diluted ownership.

Step 3: Remove unallocated ESOP

Unallocated pool shares do not participate in exit proceeds.

The 10.73% unallocated ESOP portion is removed, and its economic share is redistributed proportionally among actual shareholders. This creates payout-adjusted ownership percentages.

Step 4: Pro-rata distribution of remaining proceeds

After removing unallocated ESOP, the new effective ownership is:

These adjusted payout percentages determine how the remaining $48M is split.

Step 5: Final proceeds distribution

Pro-rata distribution of $48M (after paying Seed’s $2M preference).

The table above shows both the Seed investor’s liquidation preference amount ($2M) and their pro-rata share of the remaining proceeds. This is only for explanation. Under a 1x non-participating preference, the investor receives either the preference or the converted common payout, whichever is higher.

If the investor held 1x participating preferred. They would receive the $2M preference and then also participate pro-rata in the remaining proceeds. This is a “double dip” structure.

How cap table scenario analysis helps you plan future funding

Cap table scenario analysis gives founders, finance teams, and investors a forward-looking view of how the company’s ownership will evolve as it raises more capital. Instead of relying on rough estimates or back-of-the-envelope calculations, scenario modeling allows you to simulate how future rounds, valuation changes, ESOP adjustments, and investor terms will affect dilution and control.

A well-structured scenario model can answer questions such as:

- How much dilution will founders face if they raise a larger or smaller round?

- What happens if the company raises multiple SAFEs before a priced round?

- How do different valuation caps or discounts change investor ownership after conversion?

- What does the cap table look like if the ESOP pool needs to be increased?

- How will ownership shift across a Seed, Series A, and Series B sequence?

By simulating these outcomes, you can compare different pathways side by side and choose the one that best supports long-term growth.

Best tools for modeling ownership and dilution scenarios

Most teams rely on one of two approaches: spreadsheets or a dedicated equity management platform.

1. Spreadsheets (excel or google sheets)

Spreadsheets are great when your cap table is small and straightforward. But once you introduce multiple SAFEs, option-pool adjustments, or an upcoming priced round, spreadsheets start breaking down.

Each new assumption forces manual updates across tabs, ownership shifts with every formula change, and a single broken reference can distort the entire model. As your structure gets more complex, keeping everything accurate becomes harder and riskier.

For any company preparing for real fundraising or managing several investor classes, spreadsheets eventually hit their practical limits. A purpose-built cap table system becomes the safer, more reliable choice.

2. Dedicated equity management platforms (EquityList)

Equity management software like EquityList offers a far more reliable and structured way to run scenario models. Instead of rebuilding formulas or duplicating spreadsheets, you start directly from your live, compliant cap table and build simulations with just a few inputs. Each scenario layers on top of your actual share structure, so the results stay consistent with how your cap table really works.

From the scenario modeling module, you can:

- Start from a clean, real-time snapshot of your cap table

- Create simulations for new fundraising rounds, option pool expansions, or pool creation

- Compare ownership before and after each round in a single screen

- Enter round details such as raise amount, pre-money valuation, and option-pool targets

- Add multiple instruments to a scenario (venture debt, convertible note, equity rounds)

- See updated ownership for every stakeholder instantly as assumptions change

When it comes to how SAFEs and notes convert, EquityList keeps that logic in a dedicated conversion modeling module.

For companies raising multiple SAFEs, preparing for a priced round, or managing cross-border shareholders, dedicated tools like EquityList become essential. They remove manual complexity, prevent broken-model risks, and give founders clear visibility into how each decision affects dilution and ownership.