.avif)

Many startups include stock options through Employee Stock Option Programs (ESOPs) as part of job offers and retention packages. These stock options serve as long-term financial incentives for employees, motivating them to enhance the company's value.

The idea of being a part-owner of something is appealing because of the life-changing outcomes that equity can provide.

For example, early employees of companies like Uber and WhatsApp reaped substantial rewards when these companies went public or were acquired. Notably, the first 3,000 employees at Facebook collectively made around $23 billion at the time of its IPO. This translates to an average windfall of approximately $7.7 million per employee.

With the possibility of such high rewards, stock options also carry risks. The value of equity ownership depends on the company's performance at exit. If the terms of the exit are unfavorable, it can result in shareholders receiving far less than anticipated—or potentially nothing at all.

Types of equity compensation

While ESOPs are one of the most popular forms of equity compensation, some companies also issue SARs and RSUs to its employees.

1. Employee Stock Option Programs (ESOPs)

Stock options issued via Employee Stock Option Programs (ESOPs) are a form of compensation that grants employees the right to purchase shares of their company's stock at a predetermined price, known as the strike price.

These options come with a vesting period, after which employees can exercise them to purchase company shares at the strike price. If the company’s stock price rises above the strike price, employees can buy shares at a discount, offering them the potential for significant financial gains.

2. Restricted Stock Units (RSUs)

Restricted Stock Units (RSUs) are company shares promised to employees as part of their compensation.

Employees don’t own RSUs until they vest, and once vested, they can receive actual company shares or a cash equivalent. RSUs usually convert into shares during liquidity events, such as an IPO or acquisition, giving employees access to stock or cash value at that time.

3. Stock Appreciation Rights (SARs)

Stock Appreciation Rights (SARs) are similar to RSUs in that they provide the cash value of the stock but do not result in actual stock ownership.

Employees receive a cash payment equivalent to the appreciation in stock value over a specified period, usually from the grant date to the exercise date.

SARs do not result in stock dilution for existing shareholders, as they are settled in cash rather than additional shares.

Common shares vs preferred shares

As we explore different types of equity compensation, it’s important to understand that the shares granted through these plans are typically "common shares," which are usually given to founders and employees.

On the other hand, investors generally receive "preferred shares," which come with certain advantages like liquidation preference.

Liquidation preference determines the payout order in the event of a company's sale, liquidation, or other liquidity events. It gives preferred shareholders the right to receive their investment back (or a multiple of it) before common shareholders are paid.

For example, if an investor has a 1x liquidation preference, they get back the amount they originally invested before any proceeds are distributed to common shareholders. If they have a 2x liquidation preference, they receive double their investment before common shareholders receive any payout.

If your company performs well and grows significantly in value, you typically won’t need to worry about a queue for your equity payout. In a successful exit, investors often choose to receive their proportional share of the proceeds (based on their equity stake) rather than invoking their liquidation preference because they stand to gain more this way.

The option lifecycle

1. The company creates an option pool

When a company begins seeking external funding, they typically set aside an employee option pool. This pool usually makes up 10-15% of the total equity at the seed stage and can grow to around 20% by Series D.

Founders allocate equity from this pool to early employees as they join. However, after the initial hiring phase, usually from Year 2 onwards, stock options are awarded more selectively during performance appraisals to recognize and reward employee commitment.

2. Employees are offered options

As employees receive options from the pool, it’s important to remember that these are not actual company shares yet. Options give holders the right to purchase shares in the future at a predetermined price.

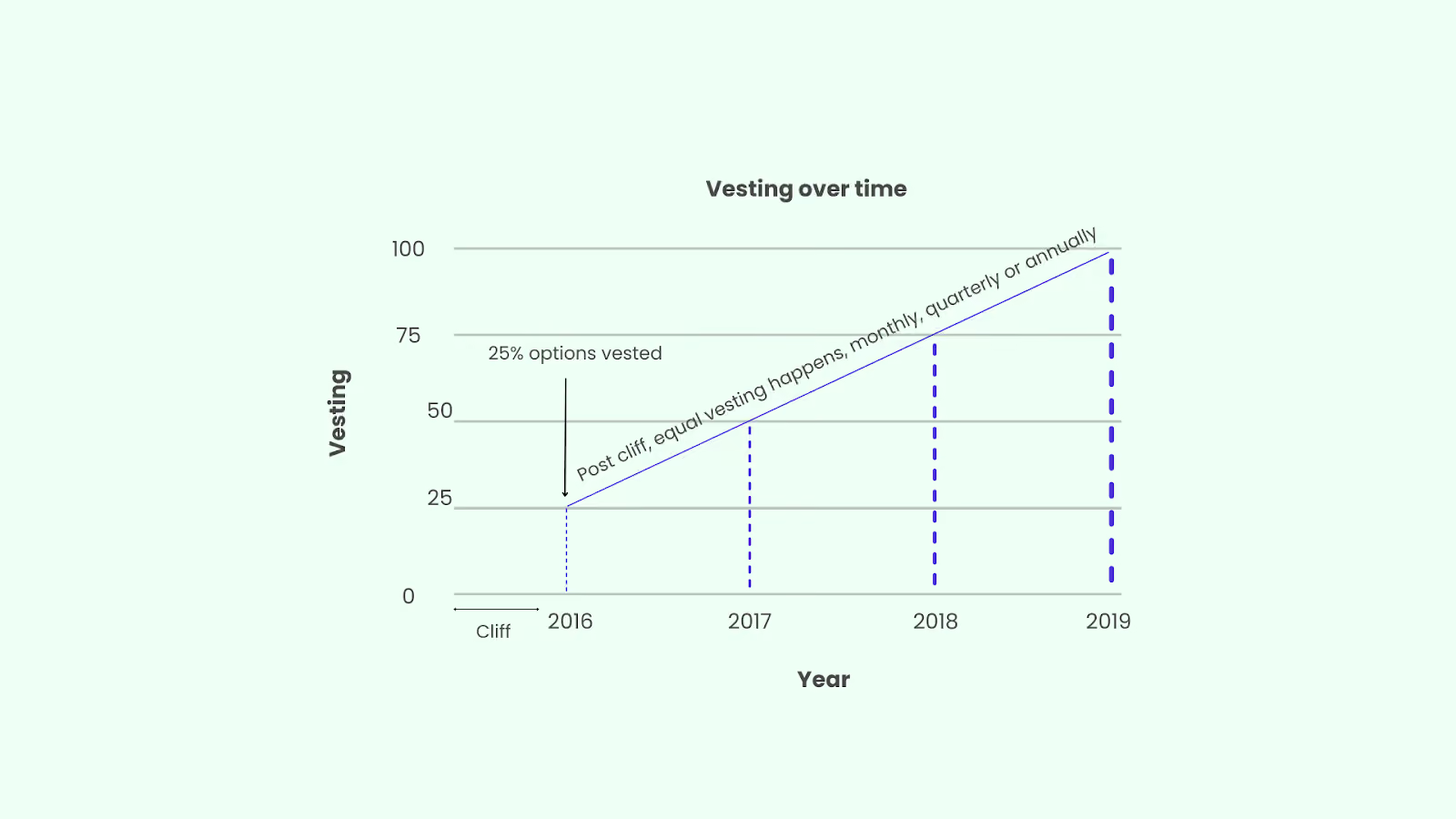

Options are also subject to a vesting schedule, which is the period over which they are granted.

The most common vesting period is four years, often with a one-year cliff. Once the cliff period ends, the options allocated during that time become available to the employee, and vesting continues according to the specified schedule—typically on a monthly, quarterly, or annual basis.

3. Vesting of options

At the end of the vesting period, which typically lasts four years, employees fully own their options.

However, exercising these options is subject to company policy. While some companies allow employees to exercise their options as they vest, others prefer to wait until a liquidity event.

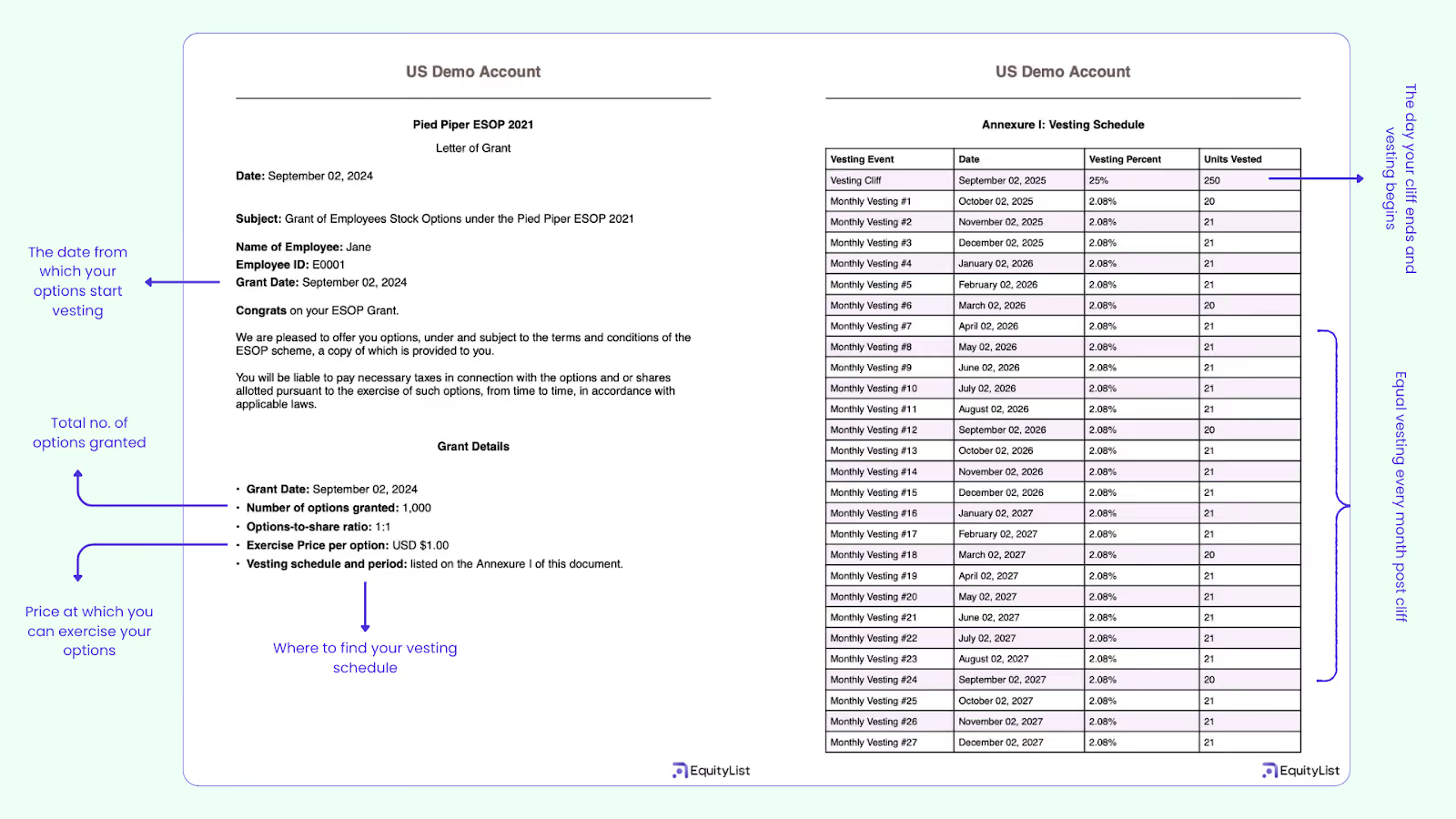

When employees decide to exercise their options, they purchase shares at a predetermined price known as the strike or exercise price, as specified in their grant letter.

See the full example grant letter template here.

4. Exercising of options

If an employee acquires the share of a company by exercising their options, they become a shareholder on their cap table.

However, to realize the gains from the difference between the strike price and the current market value of the shares, the employee will have to sell their shares in a liquidity event.

As private companies, these shares are not tradeable on public markets, meaning employees must wait for an IPO or acquisition for potential payouts. Some companies offer Stock Repurchase Programs (buybacks or secondary sales), allowing employees to sell shares back to the company or investors before a major exit event.

For instance, Urban Company (formerly known as UrbanClap), an on-demand home services platform founded in 2014, organized its first cashout in June 2017 during its Series C funding round. At that time, UrbanClap’s shares were valued at $337 (INR 24,000) per share.

In November 2018, they announced a second ESOP and share cashout worth $2 to $2.5 million (INR 14 to 18 crore) at $871 (INR 62,000) per share during their $54 million Series D funding. Reportedly, around 50 of the 100 eligible employees exercised their options to sell their shares.

Other companies, like Flipkart, Ola, Razorpay, and Swiggy, have also executed buybacks in the past.

While you could exercise your options as soon as they begin to vest, many people prefer to wait until the exit time (or until a “Secondary Sale” or Buyback is offered by the company) to exercise their options. This strategy helps delay tax liabilities until necessary.

The costs and taxes incurred from exercising options are deducted from the proceeds you realize from the fair market value (FMV) of your shares at the time of exit. You can calculate your returns using this formula:

(Number of options * (Price per share - Strike price)) - Taxes

Taxes on ESOPs

When you exercise stock options, you receive income in the form of shares, making you liable for taxes on that income.

Understanding the tax implications can be complex, especially since they vary based on when you choose to exercise your options—whether during a liquidation event or beforehand.

Exercising before a liquidation event

If you decide to exercise your options before a liquidation event, you will incur tax liabilities in two parts: once when you exercise the options and again when you sell the acquired shares.

1. Upfront costs

When you exercise your options, you must pay the exercise cost plus taxes (income tax) on the difference between the current fair market value (FMV) of the shares and the strike price. The tax is calculated as follows:

Tax liability = FMV - Exercise price

2. Selling the shares

When you eventually sell these shares, you will again be liable for taxes on the difference between the selling price and the acquisition price. For example, if you exercised 1,000 stock options at Rs. 10 per share in 2018 when their FMV was Rs. 100 per share, you’d owe taxes on the Rs. 90 per share difference at that time.

Later, if you sell these shares at Rs. 500 per share during an IPO in 2020, you’ll be liable for capital gains tax on the Rs. 400 profit per share.

Exercising during a liquidation event

If you choose to exercise your options during a liquidation event, you will incur costs only once, and you may not even need any cash input upfront.

In this scenario, you pay the strike price to exercise the options and simultaneously sell the shares at a higher valuation (FMV). Your tax liability will only be on the difference between the FMV and the strike price, and this is treated as normal income tax.

Profit calculation:

Profit = Payout - Exercise cost - Taxes

One advantage of this approach is that you can easily calculate the exact expenses before making any decisions. However, this overview is not exhaustive or tailored to your specific tax situation, so seeking expert advice is recommended before exercising your options.

Know how stock options are taxed in the United States and India.

We hope you found this post helpful, do reach out to us if you have any questions.

.png)