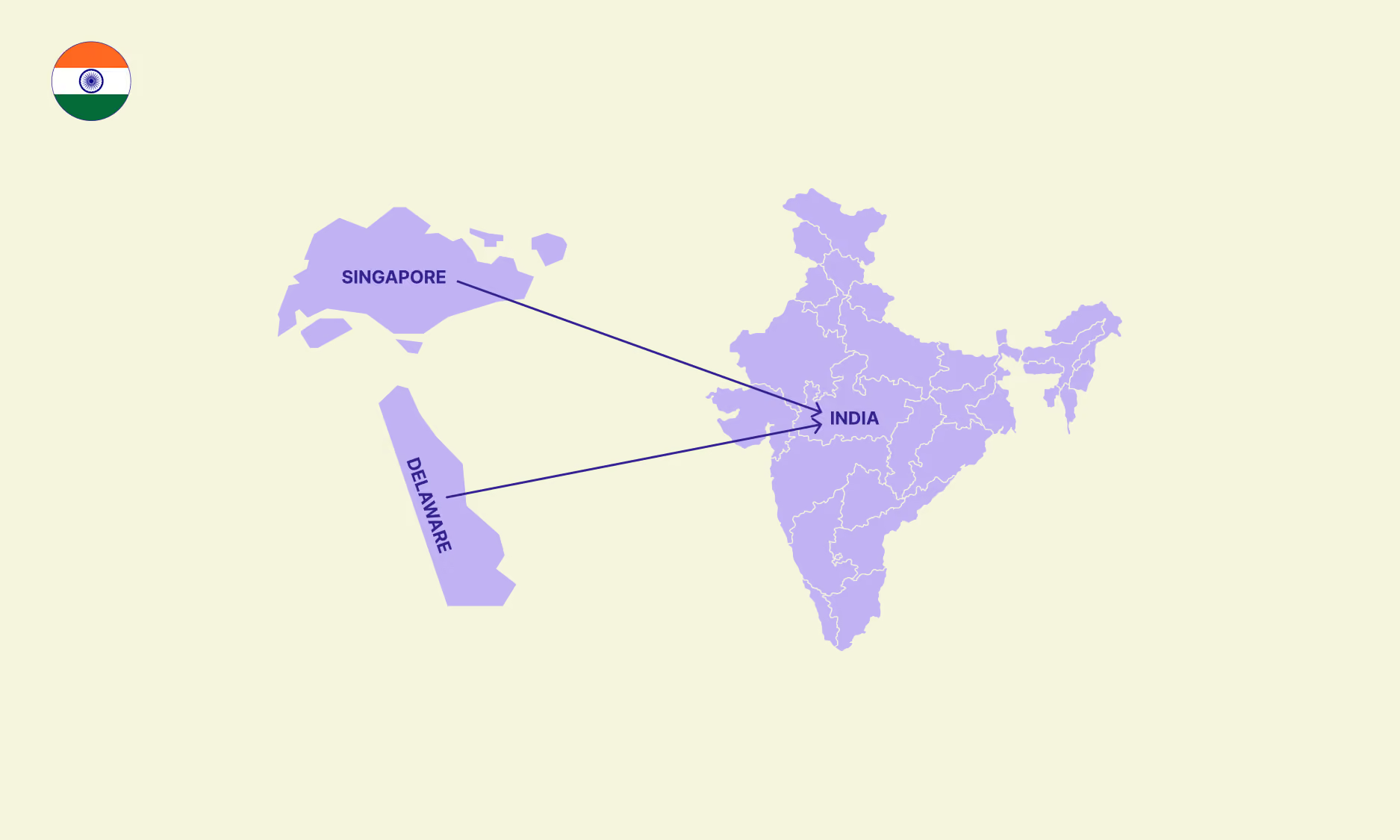

For years, many Indian startups flipped their corporate structures abroad. They incorporated in Delaware or Singapore to attract global capital, benefit from lenient regulations, access tax advantages, or tap into international IPO markets.

But that trend is reversing.

We’re now seeing a wave of reverse flipping. It is the process of shifting a startup’s holding company and control structure back to India.

What is reverse flipping?

Reverse flipping, also known as “internalisation”, is when an Indian startup that was originally flipped to a foreign jurisdiction (like the US or Singapore) restructures itself to bring its ownership, control, and legal headquarters back to India.

Startups like PhonePe, Groww, Pepperfry, and Zepto have completed this shift in the last couple of years.

Why are companies reverse flipping?

Reverse flipping is a strategic decision, especially for those companies planning to go public.

1. Easier path to IPO

India’s IPO landscape has evolved to accommodate tech-first, capital-light startups that don’t always follow the traditional path.

Unlike older businesses that went public after decades of profitability, today’s startups can list without being profitable, as long as they have a sustainable business model, clear use of funds, and strong operational metrics.

SEBI now looks at a mix of financial and non-financial indicators like GMV, customer growth, and EBITDA, especially for new-age companies.

This shift in approach has made the IPO route more accessible to startups in India.

2. Higher multiples in India

Startups listing in India often command 30–50% higher multiples, driven by a scarcity premium, stronger brand recall, and high investor enthusiasm for homegrown tech stories.

For sectors like e-commerce, fintech, and broking, where the customer base and value creation are largely domestic, listing locally increases investor relatability and brand visibility.

3. Stronger investor confidence in India-domiciled companies

Global investors are now more comfortable investing in India-domiciled startups than they were a few years ago. A growing number of successful tech IPOs has created a clear, repeatable playbook for going public in India. As a result, the need for an overseas parent company to attract funding has significantly decreased.

4. Reverse flipping is more viable now

Reforms by the RBI and the Ministry of Corporate Affairs have made the process less cumbersome.

The fast-track merger route for wholly owned subsidiaries has cut down the need for lengthy tribunal approvals. Meanwhile, updates to FEMA and income tax rules have brought clarity on key issues such as capital gains, indirect transfers, and ESOP treatment.

Common structures for reverse flipping

There are two primary ways Indian startups are executing their move back to India: inbound merger and share swap.

1. Inbound merger

In this structure, the foreign holding company merges into its Indian subsidiary, and the shareholders of the foreign company receive shares in the Indian entity. After the merger, the Indian company becomes the new parent.

a. Regulatory compliance for inbound merger

This route is governed by Section 234 of the Companies Act, 2013, and the RBI’s Cross Border Merger Regulations, 2018. In September 2024, a key amendment to the Companies (Compromises, Arrangements and Amalgamations) Rules, 2016 made this process faster for companies where the foreign entity is a wholly owned parent of the Indian subsidiary. In such cases, the merger can now happen through a fast-track route bypassing the National Company Law Tribunal (NCLT) although RBI approval is still mandatory.

Like any cross-border merger, the process requires:

- Valuation of both entities based on internationally accepted methods

- Regulatory filings with the Ministry of Corporate Affairs (MCA)

- FEMA compliance, especially where the foreign entity is from a land-bordering country (as covered under Press Note 3)

b. Tax benefit under inbound merger

If the merger qualifies as a proper “amalgamation” under Sections 47(vi) and (vii) of the Income Tax Act, it can be tax-neutral.

Tax losses from the foreign entity can also be transferred to the Indian company under Section 72A, but only if the foreign business qualifies as an “industrial undertaking”.

On the Indian side, if the merger leads to a significant change in the Indian company’s ownership, the company may lose the ability to carry forward its past tax losses under Section 79 of the Income Tax Act.

2. Share swap

Under the share swap method, shareholders of the foreign parent company swap their shares for equity in a newly created Indian company. This new Indian company becomes the direct owner of the foreign entity. At this stage, both companies remain legally separate, but the control shifts to the new Indian company.

Once this is done, the foreign company is no longer needed as a holding structure. The company is then liquidated, and its shares in the Indian operating company are distributed to the Indian parent.

The result is that the new Indian company now directly holds the Indian operating company and acts as the legal and financial parent.

a. Regulatory compliance for share swap

This route is governed by the Foreign Exchange Management (Overseas Investment) Rules, 2022.

If the Indian company operates in a sector where foreign investment is allowed without prior government approval (known as the automatic route), it can issue shares to foreign investors in exchange for their shares in the offshore company.

However, if the company doesn’t fall under the automatic route, it will need to get prior approval from the relevant regulatory body before proceeding with the share swap.

A share swap transaction must follow these rules:

- The share value must be based on a fair market valuation

- Sectoral caps (investment limits) must be respected

- Entry route restrictions (automatic vs approval) must be followed

- Filings must be made with the RBI and Ministry of Corporate Affairs (MCA)

b. Tax implications of share swap

Unlike inbound merger, share swap is not automatically tax-free.

- The exchange of shares is treated as a transfer, which may trigger capital gains tax in India, especially if the foreign entity derives value from Indian assets (as per Section 9(1) of the Income Tax Act).

- Some relief may be available under Double Taxation Avoidance Agreements (DTAAs), depending on the investor’s country of residence.

- If the foreign entity is liquidated and its assets (such as shares in the Indian company) are distributed to the Indian parent, the portion equal to accumulated profits of the foreign entity may be taxed as a deemed dividend under Section 2(22)(c) of the Income Tax Act, while the excess value may be taxed as capital gains under Section 46(2).

Why reverse flipping is an equity ops challenge

Reverse flipping brings significant complexity to how your equity is managed, tracked, and reported.

Companies often have multiple share classes and investor rights structured under foreign law. When bringing the structure back to India, everything needs to be reworked to align with local regulations while keeping investor terms intact.

Then there’s ESOP migration. Grants issued by the offshore parent often need to be cancelled and reissued by the Indian entity.

Startups flipping back from the US or Singapore often transition from ASC 718 or Rule 701 to Ind AS 102 for equity expense reporting.

.png)

.png)