What are fully diluted shares?

Fully diluted shares represent the total number of common shares of a company, which includes both outstanding shares (shares currently held by shareholders) and shares that could be obtained from the conversion of preference shares, stock options, warrants, SAFEs, convertible notes, etc:

1. Stock options

Often offered to employees or executives, stock options grant the right to purchase company shares at a predetermined price (exercise price or strike price) within a specified timeframe. When employees exercise options, they are issued common shares on the basis of the ‘options-to-share’ conversion ratio.

2. Convertible preferred stock

Certain classes of preferred stock may carry the option to be converted into common shares at various conversion ratios, such as 1:1 or 1:2, under specific conditions, such as during a merger, acquisition, when the company goes public, or at the discretion of the shareholder.

3. SAFEs

When a SAFE converts, the investor receives a predetermined number of shares based on the conversion price and the amount invested. These newly issued shares are included in the fully diluted share count.

4. Convertible notes

Similar to SAFEs, upon conversion, convertible notes are exchanged for shares at a predetermined price. The number of shares issued through this conversion is added to the fully diluted share count.

5. Warrants

Similar to stock options, warrants are financial instruments that entitle the holder to buy company shares at a predetermined price within a specified period. They are commonly issued to investors, employees, or as part of debt agreements. Warrants can be exercised to convert into common shares, thereby contributing to the fully diluted share count.

Analyzing fully diluted shares is critical. It reveals the maximum dilution for existing shareholders and its impact on the company's capital structure. This insight empowers investors to assess the potential future ownership landscape and its effect on shareholder value.

How do fully diluted shares work?

To calculate the fully diluted shares, you need to consider several factors that could impact the total share count a company might have in the future:

1. Outstanding shares

Outstanding shares represent the total number of shares of a company's stock that are currently held by shareholders.

This includes shares held by:

- Individual investors

- Institutional investors

- Founders, employees, and board members

They represent the baseline for the company's ownership structure and serve as the starting point for calculating fully diluted shares.

2. Shares from convertible securities

When calculating fully diluted shares, the potential number of shares resulting from the conversion of convertible securities, such as convertible notes, SAFEs, or convertible preferred stock, is added. This reflects the impact of potential future conversions in the company's ownership structure.

3. Stock options

Stock options give employees or executives the right to buy company shares at a set price (exercise price) within a specific timeframe. These options are factored into the fully diluted share count, even if they haven't been exercised yet.

Why? Because if employees do decide to exercise their options, they become shareholders, acquiring common shares. This increases the total number of shares outstanding, which dilutes (reduces the ownership stake of) existing shareholders.

When building a fully diluted cap table, you consider both:

- Total outstanding options: This includes all options that have been granted, regardless of whether they've been exercised.

- Unallocated options: These are options that haven't yet been granted to specific individuals.

By including both outstanding and unallocated options, the fully diluted share count provides a more complete picture of potential ownership dilution.

4. Potential shares from warrants

Similar to stock options, warrants provide the holder with the right to purchase company shares at a predetermined price. When warrants are exercised, they contribute to the issuance of new shares. Including the potential shares from exercised warrants in the fully diluted share count account for the impact of warrant conversions on the company's ownership structure.

Impact of fully diluted shares

The impact of fully diluted shares extends beyond just numerical calculations. It affects key financial metrics and investor perception in several ways:

1. Ownership dilution

As convertible securities, stock options, and warrants are exercised or converted into shares, new shares are issued, diluting the ownership percentage of existing shareholders. Fully diluted shares reveal the maximum potential dilution of ownership, allowing investors to make informed decisions about their long-term stake in the company.

2. Earnings Per Share (EPS)

For listed companies, EPS is a crucial metric used to evaluate a company's profitability. A higher number of fully diluted shares leads to a lower EPS, as earnings are spread across a larger number of shares. This can make the company's stock appear less valuable on a per-share basis, potentially affecting investor sentiment and stock valuation.

Example of fully diluted shares

Let's consider a hypothetical example to illustrate fully diluted shares:

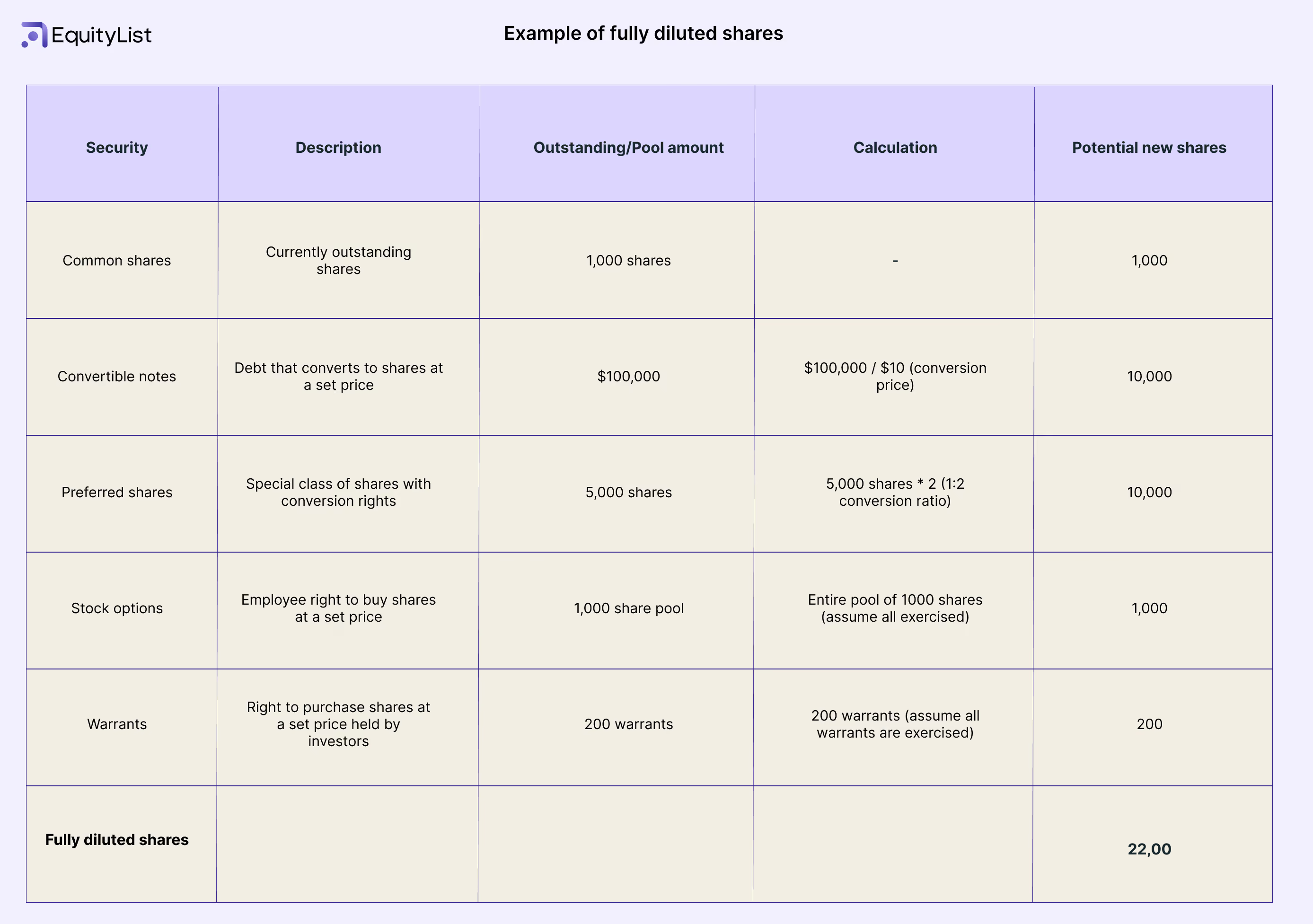

Company ABC currently has 1,000 outstanding shares.

Dilutive securities

1. Convertible notes

Company ABC issued a $100,000 convertible note with a conversion price of $10 per share. Upon conversion, this note would convert to 10,000 shares. ($100,000 / $10 = 10,000 shares)

2. Preferred shares

The company also issued 5,000 preferred shares with a 1:2 conversion ratio to common stock. This means each preferred share can be converted into 2 common shares. (5,000 preferred shares * 2 conversion ratio = 10,000 potential common shares)

3. Stock options

The company also has a total stock option pool of 1,000 shares with an exercise price of $15 per share. Currently, 500 options of the total pool of 1,000 shares have vested and been exercised by employees.

Since we have a total pool of 1,000 options and 500 have been exercised, we have 1,000 - 500 = 500 unexercised options. However, for fully diluted shares, we assume all options are exercised, so we consider the total pool (1,000 shares).

4. Warrants

Investors hold warrants to purchase 200 shares at an exercise price of $20 per share.

Here’s how to calculate fully diluted shares for the above company

- Outstanding common shares: 1,000 shares

- Shares from convertible notes: 10,000 shares

- Convertible preferred stock: 10,000 shares

- Total stock options pool: 1000 shares

- Potential shares from warrants: 200 shares

Total fully diluted shares = 1,000 + 10,000 + 10,000 + 1,000 + 200 = 22,200 shares

22,200 shares represent the total number of shares the company would have if all convertible securities, exercised stock options, and warrants were converted or exercised

Outstanding shares (basic shares) vs fully diluted shares

Let’s summarize what we learned above.

Basic shares and fully diluted shares represent different aspects of a company's share structure, especially concerning potential future ownership and financial metrics. Let's break down the differences:

1. Outstanding shares (basic shares)

a. Outstanding shares refer to the total number of shares outstanding at a given point in time. These can be common shares or preferential.

b. These are the shares currently issued and available for transactions in the form of secondary trades and buybacks.

c. Outstanding shares do not account for potential future dilution from convertible securities, such as stock options, warrants, convertible notes, convertible preferred stock etc.

d. They are used to calculate financial metrics like earnings per share (EPS) and are often reported in financial statements and disclosures.

2. Fully diluted shares

a. Fully diluted shares represent the total number of common shares a company would have if all potential dilutive securities were converted into shares.

b. They provide a more comprehensive view of a company's potential future ownership structure and its impact on financial metrics.

c. Fully diluted shares are used to assess the maximum potential dilution impact on existing shareholders' ownership and to calculate adjusted financial metrics, such as diluted earnings per share (Diluted EPS).

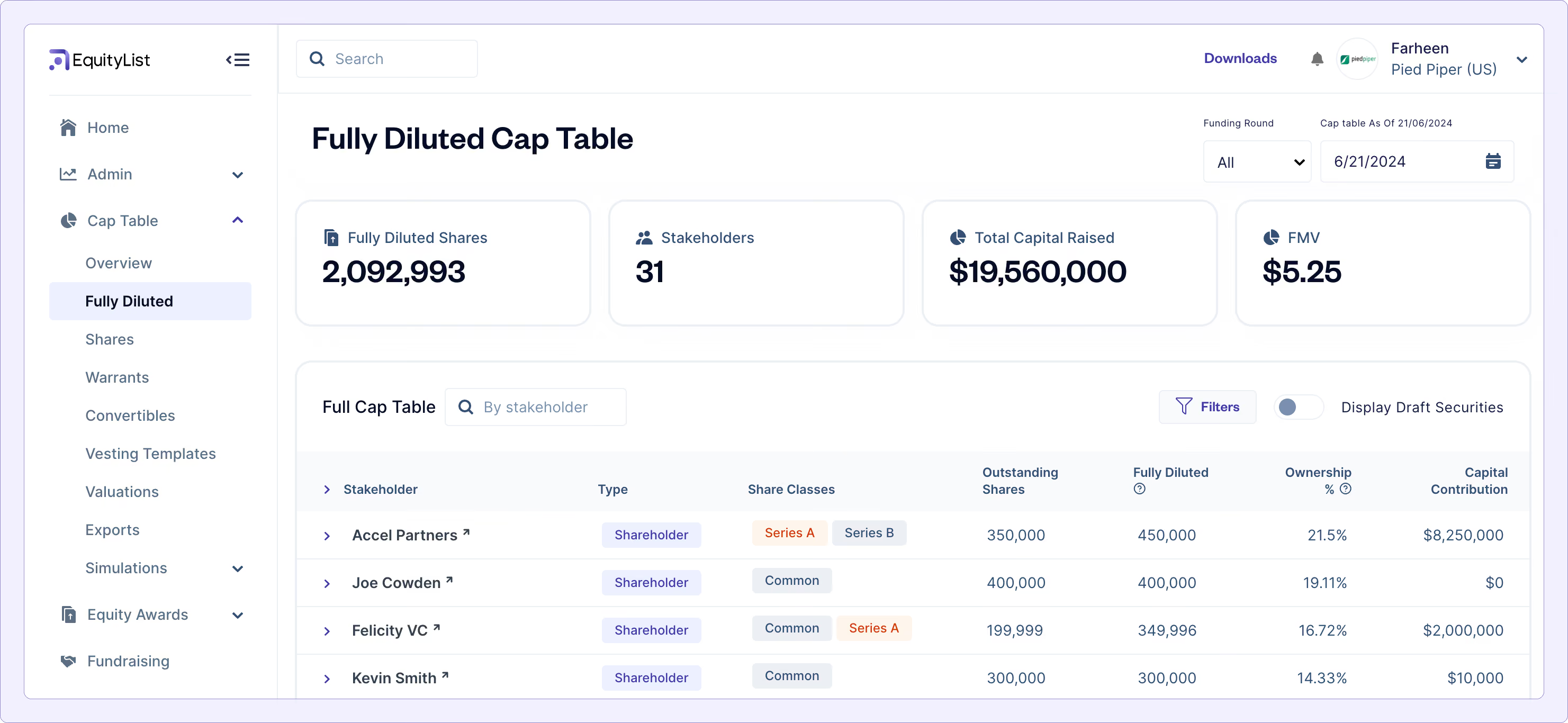

Fully diluted shares on EquityList

Companies often issue dilutive securities such as preferred stock to investors, Employee Stock Option Plans (ESOPs) to incentivize employees, and convertible notes to raise capital quickly. Failing to account for these potential future issuances of securities can lead to an inaccurate fully diluted cap table, impacting the founders' ownership percentages, as they may unknowingly give up more equity when these securities convert.

At EquityList, we recognize the importance of founders understanding their complete ownership structure. Hence, our platform not only displays your outstanding cap table but also provides visibility into your fully diluted cap table. This ensures founders, the company’s shareholders, and incoming investors have a comprehensive view of potential dilution effects from all outstanding securities, empowering stakeholders to make informed decisions about equity management.

Check out EquityList.