VC deals operate like gears, shifting depending on the state of the economy. In good times, founders have the upper hand. They can negotiate for larger investments, maintain more control over their company, and select investors who share their vision. This often leads to more favorable terms for founders, such as a lesser equity dilution, lower liquidation preference of 1X and limited or no pro-rata rights. Pro-rata rights give investors the option, but not the obligation, to participate in future financing rounds.

However, during economic downturns, investors hold more sway. This results in negotiations with significantly different terms. Investors might seek a higher liquidation preference of 2X or more and request anti-dilution protection. Anti-dilution provisions safeguard an investor's equity stake from dilution in case of a down round. They may also push for aggressive drag-along rights, which compel founders to sell their shares if a buyer emerges. Additionally, investors may insist on tag-along rights, allowing them to sell their shares proportionally if founders sell a majority stake.

During negotiations, founders may not fully anticipate the long-term implications of the agreed-upon terms, potentially exposing the company to greater risk.

For instance, let's consider a scenario where a startup agrees to a 2X liquidation preference in a challenging market. This means that the investor receives double their initial investment before any profits are distributed to the founders, employees, or other shareholders.

Now, imagine the startup is acquired for $6 million, but after settling debts and other obligations, only $4 million remains. With a 2X liquidation preference, the investor would be entitled to their $2 million first. Consequently, only $2 million would be left to be divided among all shareholders. This significantly reduces the founders' payout.

Therefore, it's crucial for founders to use cap table modeling to visualize the future implications of such terms during negotiations.

What is cap table modeling?

Cap table modeling is a fundamental tool used by companies to project their ownership structure over time. It involves analyzing various components of the company's ownership, including:

1. Equity ownership

Equity ownership is determined by the percentage of shares held by each shareholder relative to the total outstanding shares, on a fully diluted basis which means converting all types of preferred shares into equity shares. This calculation is crucial for assessing ownership distribution and new equity issuances to investors with complex structures, such as warrants, options, or convertibles, can complicate it.

Example:

- A company has 100,000 outstanding shares.

- The founders collectively own 60% of the company, while early investors hold 20%, and the balance 20% is for employee stock options.

New funding round:

- The company seeks additional funding and negotiates with a VC to invest $5 million in exchange for 25% equity ownership in the company at the share price of $150 per share.

- However, the VC also requested warrants, allowing them to purchase an additional 500,000 shares at $160 per share within the next three years.

Impact on ownership after VC investment:

VC: 25%

Founders: 45% (diluted from 60%)

Early Investors: 15.% (diluted from 20%)

Employee Stock Options: 15% (diluted from 20%)

However, the warrants granted to VCs introduce the possibility of further dilution for existing shareholders if exercised. Therefore, companies need to model this scenario to understand the maximum dilution with VCs and have foresight when raising another round of funding to avoid excessive dilution.

2. Securities

Companies usually issue various types of securities like common stock, preferred stock, stock options, warrants, convertible notes, etc., each having different characteristics and rights. However, the characteristics of these securities are not set in stone; they are often subject to negotiation and customization during fundraising rounds.

For instance, consider a scenario where an investor negotiates to receive convertible preferred shares with a 1:2 conversion ratio, which means each preferred share can be converted into two common shares.

This would result in dilution for existing shareholders when the investor decides to execute this right. Understanding that the current stake of existing shareholders could be diluted to a certain extent based on this is important to set expectations.

3. Transactions

Transactions within cap table modeling encompass various activities, such as equity financing rounds, stock option grants, stock repurchases, and mergers/acquisitions. The structuring of these transactions on the cap table is really important.

For instance, consider a scenario where a startup, backed by a VC, is approached for acquisition by a larger competitor. In such negotiations, the presence of VC terms, like drag-along rights, can significantly influence the outcome. Drag-along rights empower majority shareholders, often VC investors, to compel minority shareholders to participate in the sale of the company.

In this context, minority shareholders, including founders and early employees, may find their ability to negotiate independently constrained by drag-along rights. Even if they believe that the acquisition terms undervalue the company or are not in their best interests, they may feel compelled to accept the deal to avoid potential legal ramifications or financial losses.

4. Valuation

Company valuations play a pivotal role within the cap table modeling, serving as a critical benchmark that guides decisions during fundraising rounds. However, the valuation process isn't solely reliant on financial metrics; it's also influenced by a multitude of factors, including investor terms, market dynamics, and regulatory considerations.

Imagine a promising tech startup gearing up for its Series B funding round to fuel expansion plans. While negotiating with potential investors, a prominent venture capital firm expresses interest but proposes a down-round, citing market uncertainties or competitive landscape concerns. However, the startup's existing investors have anti-dilution clauses in their investment agreements. The request for a down-round by new investors triggers these clauses, potentially necessitating adjustments to the conversion price or the issuance of additional shares to existing investors to offset dilution.

To put this into perspective:

Initial situation:

- Tech startup XYZ has 2,000,000 outstanding shares.

- Existing investors collectively own 20% of the company.

- Valuation: $10,000,000 ($5 per share).

Series B funding round:

- New VC proposes a lower valuation of $8,000,000 due to market uncertainties.

- They invest $2,000,000 for 25% ownership.

Existing investors' ownership is diluted to 16% but they have anti-dilution clauses and you will have to make adjustments to offset this dilution. You will have to drop their conversion price to $4 per share from the original price of $5 at which they bought the shares. This adjustment compensates for the lower valuation, allowing existing investors to maintain their ownership by issuing additional shares to them.

Types of cap table models

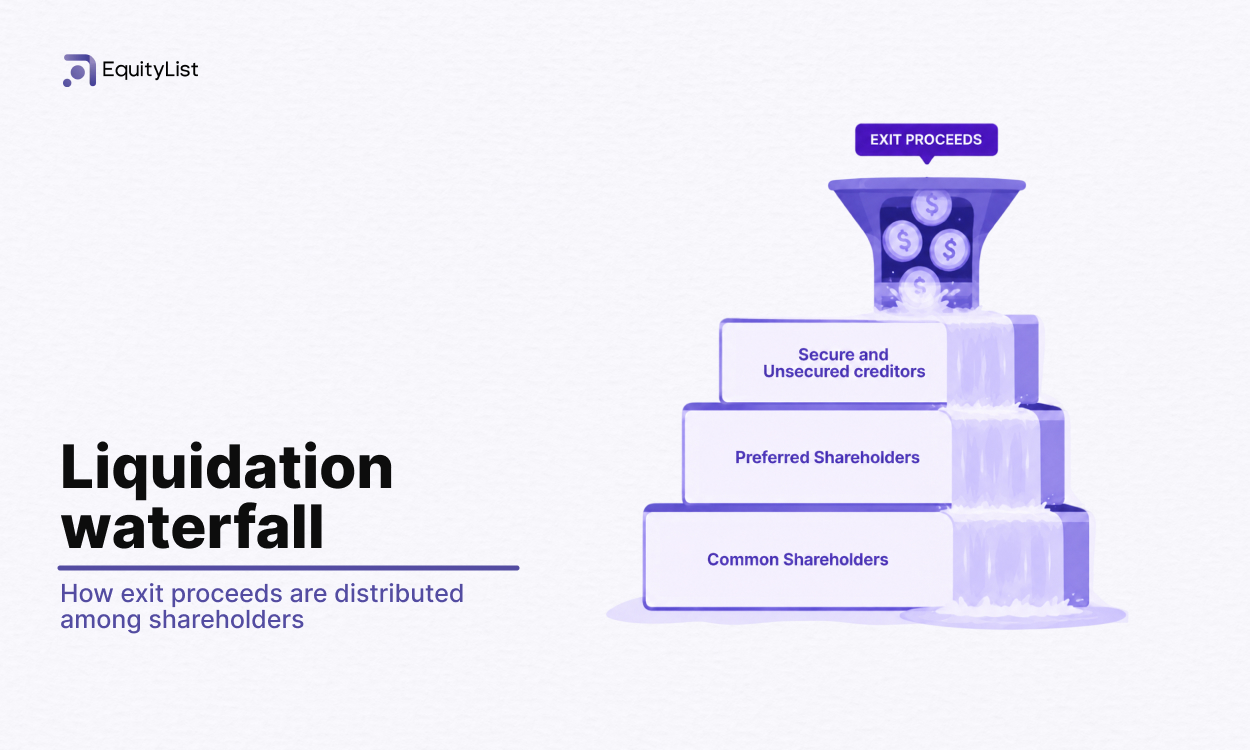

1. Waterfall modeling

Waterfall modeling is a complex financial modeling technique used to determine the distribution of proceeds from a liquidity event, such as a merger, acquisition, or IPO, among different classes of shareholders based on their contractual rights and preferences.

The term "waterfall" metaphorically describes the sequential order in which proceeds are distributed, starting from the top (most senior class of securities) and flowing down to subsequent classes in a predetermined hierarchy.

In waterfall modeling, the priority levels of each class of securities are established based on their contractual terms, such as liquidation preferences, participation rights, and conversion ratios. These terms dictate the order in which shareholders receive proceeds and the extent of their entitlement relative to other classes of securities.

For example:

Scenario:

- A tech startup is acquired for $50 million.

- The acquisition deal includes various stakeholders who are entitled to receive proceeds from the sale in a specific order.

Waterfall modeling:

- Debt holders:

- The startup has $10 million in debt.

- Debt holders are paid off first.

- Remaining proceeds: $50 million - $10 million = $40 million.

- Preferred equity holders:

- Preferred equity holders are entitled to $20 million.

- If there's insufficient remaining proceeds, they receive all available funds.

- Remaining proceeds: $40 million - $20 million = $20 million.

- Common equity holders:

- Common equity holders receive any remaining proceeds after senior debt and preferred equity.

- Remaining proceeds: $20 million.This amount is distributed among common equity holders based on their ownership percentages.

2. Conversion modeling

Conversion modeling is essential for understanding and forecasting the conversion of convertible securities, such as convertible notes or preferred stock into common stock or other equity securities.

You need to first review the conversion terms outlined in the company’s governing documents/investment agreements, which specify details like the conversion price, conversion ratio, and conversion triggers. You then calculate the conversion ratios for each convertible security, representing the number of shares obtained through conversion.

By simulating various conversion scenarios, including different conversion prices, ratios, and triggers, stakeholders can assess the potential dilutive impact on existing shareholders and the resulting implications on ownership structure and shareholder value.

For example:

Scenario:

- Tech startup ABC issues convertible notes worth $500,000 to an angel investor.

- The convertible notes have a conversion discount of 20% and a valuation cap of $5,000,000.

- The startup plans to raise a Series A round at a pre-money valuation of $10,000,000.

Conversion modeling:

Initial investment:

- Angel investor invest $500,000 through convertible notes.

Convertible note terms:

- Conversion discount: 20%

- Valuation cap: $5,000,000

Series A financing:

- Series A pre-money valuation: $10,000,000

Determine the effective price per share for the convertible notes:

With a 20% discount, the effective valuation for conversion of convertible notes = Series A pre-money valuation * (1 - Discount) = $10,000,000 * (1 - 0.20) = $8,000,000

However, the valuation cap applies if it results in a lower price per share. So, the effective price per share is the lesser of:

Series A pre-money valuation / Valuation Cap = $10,000,000 / $5,000,000 = $2 per share

Price with discount = $2 * (1 - 0.20) = $1.60 per share

The number of shares the convertible notes will convert into = Investment amount / Effective price per share = $500,000 / $1.60 per share ≈ 312,500 shares.

We understand that it can be overwhelming for you to do these analyses on your own with so many calculations, hence EquityList’s cap table management software has a built-in feature for you to model multiple events. You can check out the tool here.

3. Weighted Average Cost of Capital (WACC):

The Weighted Average Cost of Capital (WACC) is a good metric to get a broader perspective on a company’s overall capital structure and the relative weights of debt and equity. It helps figure out how much it costs a company to raise money from both debt and equity.

While WACC doesn’t have anything to do with the ownership percentages of stakeholders in a cap table, it’s important because it helps determine the cost of equity. Which further affects how investors value the company and thus eventually the value of the equity held by stakeholders.

If the cost of equity is high, future investors might lower the valuation of the company and get a bigger share of the pie at a much lower cost. As a result, stakeholders, including founders, employees, and investors, may end up with smaller ownership percentages in the company.

Let's illustrate this with an example:

Scenario:

- A tech startup has a current valuation of $10 million.

- It has raised $5 million in equity from investors, resulting in a 50% equity ownership.

- The remaining $5 million is financed through debt, resulting in a 50% debt ownership.

Calculation of WACC:

- Cost of equity: Let's assume the cost of equity is 20%. This represents the return investors expect for the risk they take by investing in the company.

- Cost of debt: Suppose the cost of debt is 10%. This is the interest rate XYZ pays on its debt.

- Weight of equity and debt: Since both equity and debt each make up 50% of the total capital, their weights are 0.5.

WACC calculation:

- WACC = (Weight of Equity * Cost of Equity) + (Weight of Debt * Cost of Debt)

- WACC = (0.5 * 20%) + (0.5 * 10%)

- WACC = 10% + 5% = 15%

Impact on future valuation:

Suppose the startup wants to raise additional funding. If the cost of equity increases to 25% due to perceived higher risk or market conditions, the WACC would rise accordingly. A higher WACC indicates higher overall cost of capital for the company. To maintain the same WACC, the startup may need to accept a lower valuation. This could result in future investors acquiring a larger share of the company at a lower cost, diluting the ownership percentages of existing stakeholders, including founders, employees, and initial investors.

What is financial modeling?

Cap table modeling is limited to projecting and analyzing the ownership structure of a company by considering all potential scenarios related to equity commitments. Financial modeling however is a broader concept to forecast the financial performance of a company, including revenue growth, profitability, cash-flow projections, etc.

It influences cap table modeling in various ways including:

1. Forecasting financial performance

Financial modeling allows companies to project their financial performance based on historical data, market trends, and assumptions. This helps anticipate the need for future financing rounds and assess the impact of these rounds on the ownership structure. It also helps in valuation exercises such as 409A, Merchant Banker (for India) etc.

2. Scenario analysis

This helps evaluate the potential impact of various events, such as changes in revenue growth, funding requirements, or market volatility on the company's financial health and ownership structure. Projecting a company's financial performance relies on analyzing historical data and current market conditions. However, scenario analysis factors in the potential impact of unexpected events or outcomes on the equity's value. We talk about this in detail in the next section.

3. Optimizing capital structure

Financial modeling helps companies optimize their capital structure by determining the most efficient mix of debt and equity financing. This optimization considers factors such as the cost of capital, risk tolerance, and capital availability, all of which play crucial roles in assessing the dilutive effects of new equity issuances and designing financing strategies that minimize dilution.

What is scenario modeling?

Scenario modeling involves creating multiple hypothetical scenarios based on different assumptions, market conditions, or events, and then analyzing the financial implications of each scenario. It helps businesses make informed decisions by understanding how changes in key variables may affect their operations, finances, and strategic goals.

Scenarios are a part of modeling, so when you model your cap table dilution as well that’s based on some scenarios. Same goes with financial modeling, you consider various scenarios for which you model your finances.

How to do scenario modeling analysis?

Here's a step-by-step guide on how to perform scenario modeling:

1. Define objectives

Determine the key questions you want to address or the decisions you need to make based on the outcomes of the scenarios.

2. Identify key variables

Identify the key factors that could influence the performance of the business. It may include market conditions, economic indicators, regulatory changes, technological advancements, and internal factors such as sales growth, expenses, or investment decisions.

3. Create scenarios

Based on the identified variables, develop different scenarios that represent plausible future conditions. Scenarios can range from optimistic to pessimistic and may include best-case, worst-case, and moderate-case scenarios. Consider the range of possible outcomes and the degree of uncertainty associated with each scenario.

4. Develop financial models

For each scenario, build financial models to project the financial performance of the business. The financial models should incorporate the assumptions specific to each scenario and calculate the expected outcomes in terms of revenue, expenses, cash flow, profitability, and other key metrics.

Types of scenario modeling

1. Baseline scenario

It represents the most likely or expected future outcome based on current trends, assumptions, and forecasts.

Example: If a manufacturing company wants to forecast its revenue and expenses for the upcoming year based on current market conditions, historical performance, and industry trends in the baseline scenario, they would assume steady economic growth, stable demand for products, and consistent operating costs.

2. Best-case scenario

This is focused on representing an optimistic future outcome where favorable conditions prevail, leading to higher-than-expected performance and results.

Example: A tech startup launches a new product and anticipates rapid adoption by consumers, leading to higher-than-expected use engagement and market share. The best-case scenario assumes enthusiastic customer demand, positive reviews, and minimal competition, resulting in accelerated revenue growth and profitability.

3. Worst-case scenario

In this scenario, a pessimistic future outcome where adverse conditions or events occur, leading to lower-than-expected performance and results is assumed.

Example: An airline company faces a severe downturn in travel demand due to a global health crisis, resulting in widespread flight cancellations, travel restrictions, and reduced passenger bookings. The worst-case scenario assumes prolonged disruptions to air travel, significant revenue losses, and heightened operational challenges, leading to financial distress and liquidity issues.

4. Moderate or base-case scenario

This represents a middle-of-the-road outcome that falls between the best-case and worst-case scenarios, reflecting a balanced view of potential outcomes.

Example: A retail chain develops a strategic plan for expansion into new markets while maintaining its existing operations. The base-case scenario assumes moderate economic growth, gradual market expansion, and manageable operating costs. It represents a balanced view of potential outcomes, neither overly optimistic nor excessively pessimistic.

In summary, cap table modeling and scenario analysis are vital tools for understanding equity financing and ownership dynamics. They empower founders to negotiate better terms, visualize the impact of different scenarios, and make informed decisions. By optimizing their capital structure and preparing for uncertainties, companies can drive sustainable growth and success.