.avif)

What is a post-money SAFE?

A post-money SAFE (Simple Agreement for Future Equity) is an agreement where the investor’s ownership percentage is calculated after all existing SAFEs are accounted for in the company’s capitalization at the time of conversion.

Based on the post-money valuation cap, it gives investors a clear, fixed percentage of ownership when their SAFE converts at the next equity financing round.

Compared to a pre-money SAFE, where ownership is calculated before considering other SAFEs, a post-money SAFE offers investors more certainty, but introduces a greater risk of dilution for founders.

Pre-money SAFE vs post-money SAFE: Key differences

As mentioned, pre-money SAFEs share dilution among founders and all SAFE investors (earlier SAFEs get diluted by newer ones), but…

Post-money SAFEs shift the entire dilution burden onto founders and existing shareholders.

Hence, modeling post-money SAFEs in your cap table is important to anticipate founder dilution, avoid overcommitting equity, and make informed decisions, especially when multiple SAFEs are stacked before your next priced round.

Why post-money SAFEs matter in cap table modeling

A post-money SAFE locks in an investor’s ownership percentage upfront, and when multiple are issued, founders risk major dilution surprises. This makes it essential to model the impact of post-money SAFEs on your cap table.

Here’s how it works: If an investor puts in $3 million on a post-money SAFE with a $30 million valuation cap, they’re entitled to 10% ownership at the time of conversion.

$3M / $30M cap = 10% ownership.

Since it’s a post-money SAFE, that 10% is fixed, regardless of how many other SAFEs are issued. This is great for investors because their stake is locked in.

However, for founders, this creates a compounding dilution effect, where each SAFE issued dilutes their own equity, not that of the other investors.

Why this matters for founders

When your priced round hits and all the post-money SAFEs convert, they won’t dilute one another — only founders, if there are no existing shareholders on the cap table. If you’ve issued multiple SAFEs without modeling them properly, you may find your founder equity has shrunk far more than expected.

Let’s say you issue:

- A $250K post-money SAFE with a $5M cap → 5% dilution

- Another $500K post-money SAFE with a $5M cap → another 10%

While each SAFE investor has their stake locked in, you (the founder) will be diluted by 15% in total. Unlike pre-money SAFEs, where dilution is shared across SAFE investors.

That’s why it’s critical to:

- Track how each SAFE affects your cap table and dilution

- Consider the aggregate dilution impact before raising a priced round

- Model SAFEs in real time using tools like EquityList

Why do modeling tools like EquityList matter?

Without proper modeling tools, it’s nearly impossible to track:

- How stacking SAFEs compounds dilution

- The true pre–priced round ownership breakdown

- The effective founder equity post-conversion

- The pressure on your option pool or hiring plans (especially if you need to expand it at the priced round)

That’s exactly why our users love EquityList.

From a clear dashboard view of the cap table to detailed SAFE tracking, it gives founders and operators full visibility, not just for current stakeholders, but for planning what’s coming next.

How post-money SAFEs dilute existing shareholders at conversion

Post-money SAFEs make it possible to predict an investor’s future ownership stake with precision. But that same predictability can become a problem for founders and existing shareholders if multiple SAFEs are issued without modeling their cumulative impact.

Let’s walk through a scenario.

From the above example, you issue two SAFEs before your Series A:

Now, assume you raise a Series A of $5M at a $20M post-money valuation.

What happens on conversion?

- Both SAFEs convert before or at the Series A.

- Because these are post-money SAFEs, Investor A gets 5%, Investor B gets 10%, regardless of each other’s presence.

- The founder’s equity is diluted by 15% from these two SAFEs.

- The Series A investors will dilute everyone further on top of that.

Modeled cap table after SAFE conversion (Pre-Series A)

Modeled cap table after Series A

Assuming Series A takes 25% equity (standard case):

A bird's-eye view like this would help you plan better and keep you informed about what the future stake would look like.

Note: Post-money SAFEs are designed to automatically convert into equity during a qualified priced round. Unlike convertible notes, there’s:

- No renegotiation at conversion

- No maturity date or interest complications

Top cap table tools to model post-money SAFEs

EquityList

EquityList is a full-stack equity management platform designed for founders, HR, and finance teams to manage complex cap tables without relying on legal intermediaries.

Trusted by over 550 companies and managing more than $4 billion in options, EquityList’s SAFE (Conversion) modeling feature is loved by its users not just for accurate calculations, but also for helping teams confidently plan and communicate ownership outcomes.

The platform provides tools to:

- manage fundraising instruments such as SAFEs and convertible notes,

- issue and track equity grants (ESOPs/SARs),

- handle valuations,

- automate compliance, and

- organize data rooms.

Key features

- Centralized dashboard for SAFEs and convertible notes: Maintain a single source of truth of all your SAFEs and convertible notes tracking. Model conversion terms by adjusting valuation caps, discounts, and interest accrual to see their impact on ownership.

- Scenario modeling: Model complex funding scenarios (including hybrid rounds with SAFEs, notes, and priced equity) to visualize how each round affects dilution and cap table structure.

- Multi-round planning: Set up successive fundraising simulations, compare different and complex rounds, and visualize exit outcomes. Understand cumulative dilution and plan your capital strategy accordingly.

- Built-in compliance tools: Maintain clean ownership records with downloadable ‘comprehensive cap table ledger’ reports. EquityList supports equity grant tracking, valuation services (including 409A and Indian valuation standards), and equity reporting such as grant vesting, pending allotment report and expense reports compliant with Ind AS 102, ASC 718 and IFRS 2.

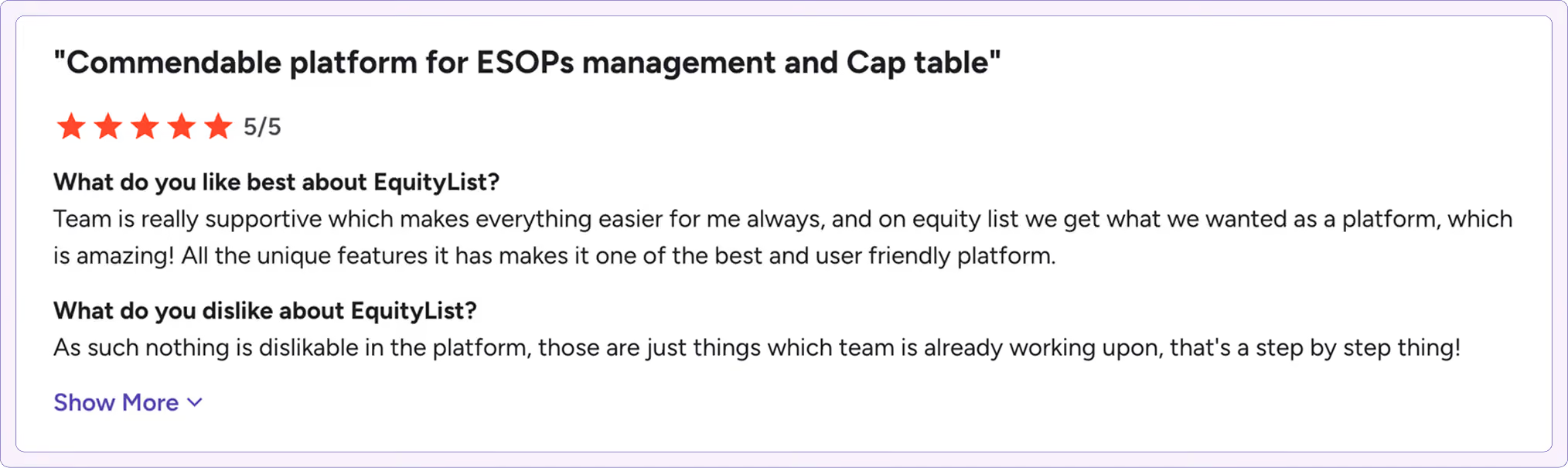

Here’s what users feel about EquityList.

Note: EquityList makes equity management accessible from day one, with transparent and predictable pricing as you grow. It’s the only platform here offering a free plan for startups with fewer than 25 stakeholders and less than $1 million raised.

Carta

Carta’s cap table management platform helps companies issue equity, track ownership, and stay financing-ready. If you’re raising a pre-seed or seed round, its SAFE modeling tools are especially useful.

You can evaluate how SAFEs and convertible notes will impact your ownership post-financing, how each instrument converts, and what terms are most favorable for your raise.

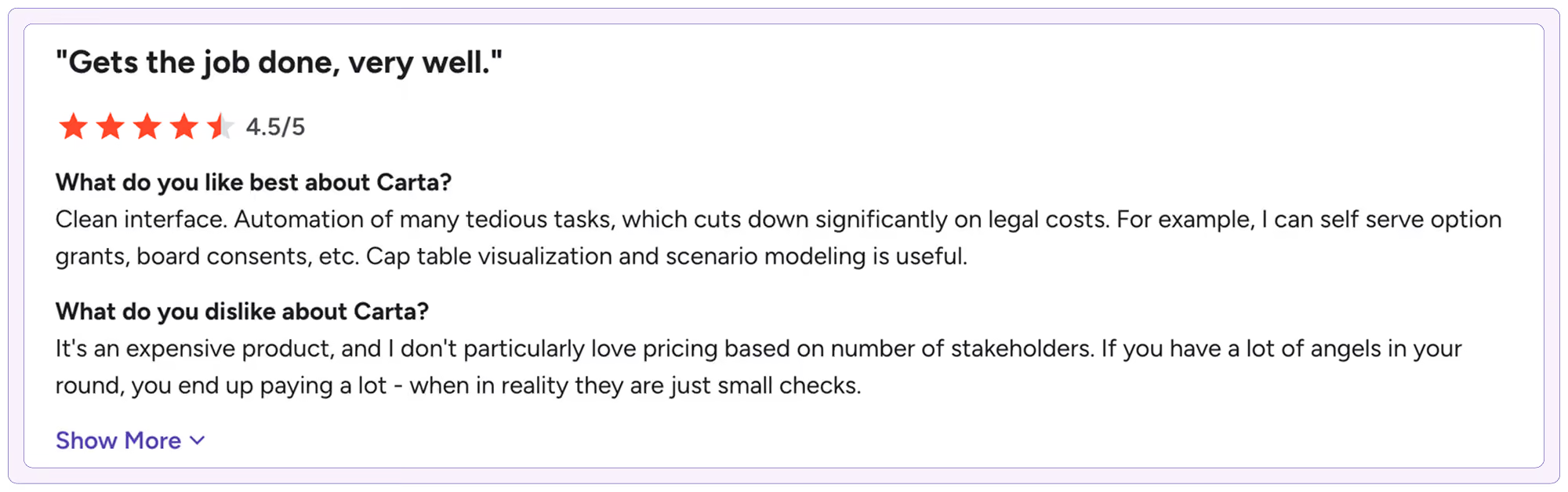

Here’s what the users have to say about the platform:

Note: While Carta does not disclose its pricing publicly, it is reportedly priced on the higher end.

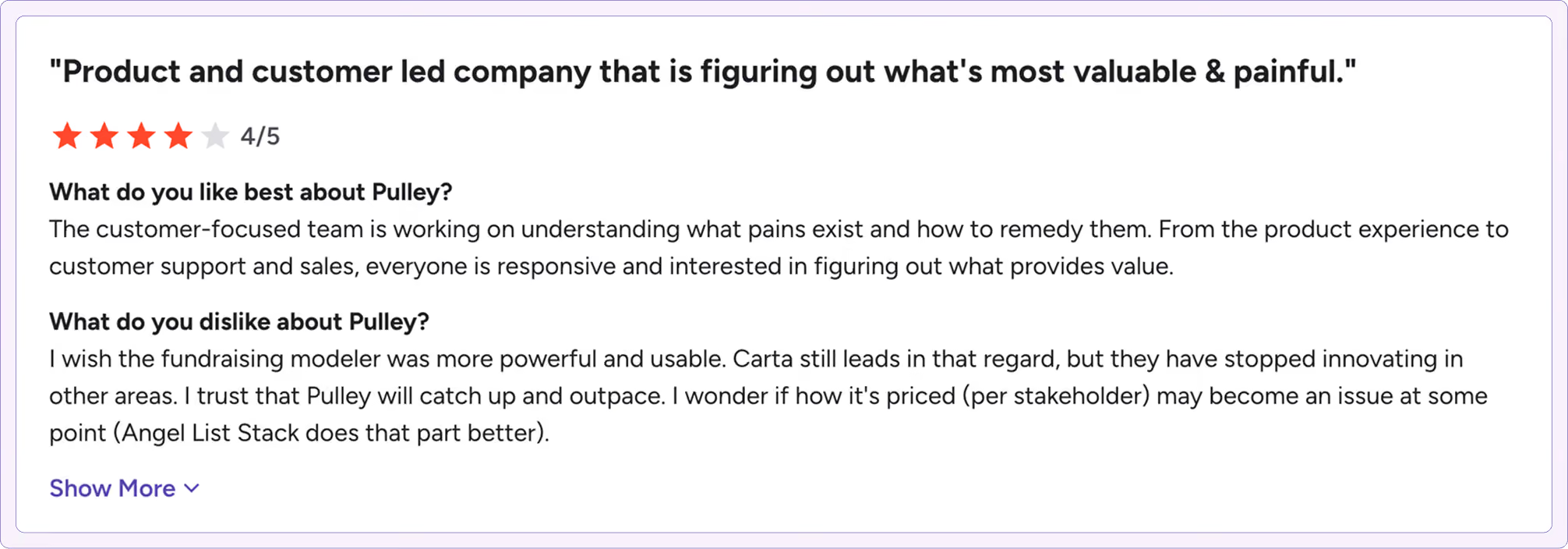

Pulley

Pulley’s fundraising modeling is purpose-built for founders and finance teams navigating pre-seed to Series A raises. It helps model dilution from SAFEs, convertible notes, and priced rounds using real cap table data.

Users can simulate pre- and post-financing outcomes, assess dilution at the stakeholder level, and generate export-ready pro formas.

Look at what users are saying about Pulley.

Note: Pulley’s paid plans start at $1,200 for up to 25 stakeholders.

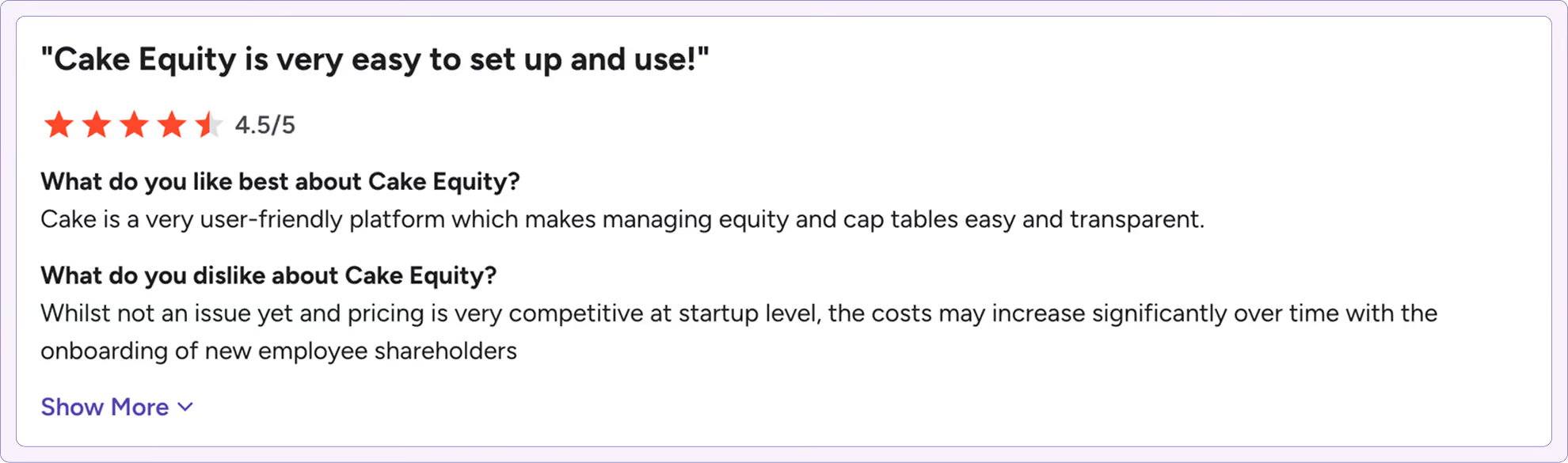

Cake Equity

Cake Equity offers a consolidated platform for managing equity, issuing shares, tracking stakeholder holdings, and streamlining fundraising workflows. Founders can simulate SAFEs, convertible notes, option pool refreshes, and priced rounds to see how each decision affects dilution and ownership.

Here’s a snapshot of a Cake Equity user review.

Note: Cake Equity does offer a free plan, but only for startups with five or fewer stakeholders.

Mistakes to avoid with post-money SAFEs

1. Forgetting to update the cap table after each SAFE

One of the most common and costly mistakes founders make with post-money SAFEs is failing to update the cap table after each issuance. Unlike pre-money SAFEs, post-money SAFEs lock in ownership percentages up front. So every time you issue a post-money SAFE, you’ve effectively given away a fixed slice of the company.

If you don’t model this in real-time, you risk stacking dilution without realizing it.

In a LinkedIn post, investor and founder advisor Shane McLean shares a hard truth:

“I see this all the time: multiple SAFE rounds at different valuations stacking up on the cap table… this habit can lead to chaos at conversion. A messy cap table and confused investors. With post-money SAFEs now the norm, it’s the founders who eat the extra dilution anyway.”

What Shane advises:

- Model ownership after conversion, not just once, but every time a new SAFE is added.

- Understand how stacked SAFEs at different caps compound your dilution.

So, keep your cap table up-to-date, clean, and scenario-modeled for investor transparency.

Use modeling tools like EquityList to simulate dilution. Sign up here.

2. Stacking up post-money SAFEs

As investor Pablo Srugo said in a LinkedIn post:

“Don’t stack post-money SAFEs. I know YC backs them & I, as an investor, love them. But for founders, 1 post-money SAFE is fine — 2+ can be deadly.”

He illustrates the danger by comparing a stack of post-money SAFEs to a deal with these investor-favoring clauses:

a. Full ratchet anti-dilution: If the next round is at a lower valuation, earlier investors get a lower price, increasing their ownership at your expense.

b. Anti-dilution against option pool expansion: If you expand your ESOP, the dilution hits only founders.

c. Anti-dilution against future SAFEs or notes: If you raise more SAFEs later, you, not the previous investors, absorb all the dilution

Always track how much ownership you’re giving away before it converts into a painful surprise.

3. Ignoring how SAFEs affect 409A valuation

SAFEs don’t require a 409A valuation when issued, but they do impact the 409A fair market value (FMV) used to price employee stock options.

409A valuations rely on a company’s fully diluted cap table and capital structure. If you’ve issued multiple SAFEs (especially with varying or aggressive valuation caps), this can skew the fair market value of your common stock.

A resulting lower FMV means cheaper exercise prices for employees. That’s great for early talent, but it can create a disconnect between internal equity pricing and external investor expectations.

Founder checklist

- Recalculate the cap table after each SAFE issuance, especially if terms vary (cap, discount).

- Update your 409A valuation regularly, especially:

- Before a priced round

- After a major SAFE round

- Prior to significant option grants

- Ensure consistency between your SAFE terms, cap table, and the valuation provider’s input.

4. Using legal templates without understanding conversion math

SAFEs are often praised for their simplicity, and that’s exactly where many founders fall into trouble. When you rely on YC-style templates without grasping the conversion math, like how valuation caps, discounts, or MFN clauses interact, you risk giving away far more equity than you intended.

If you’re not modeling each SAFE’s impact before signing, your cap table can break down at the worst time, typically during your priced round.

"The SAFE you signed might cost you your company," — A.Y., VC & Strategic Advisor

A.Y. shared a hypothetical scenario where raising $1.5M across two SAFEs quietly translated to 26.67% dilution before the Series A even closed, leaving the founder with under 50% ownership after that round (and before ESOP or co-founder split!).

His advice for founders:

- Simulate your next rounds before signing

- Cap SAFE dilution (aim for 15% or less)

- Set pro-rata limits

- Treat the cap like a valuation, because it is

Takeaway: SAFEs may look simple, but if you don't run the math correctly, they can wreck your cap table before you realize it.

FAQs on post-money SAFEs

1. What is a post-money SAFE vs pre-money SAFE?

A post-money SAFE locks in the investor’s ownership percentage based on the post-money valuation cap which includes all SAFEs issued to date. While a pre-money SAFE calculates ownership based on the valuation before accounting for other SAFES, making dilution harder to predict.

2. How do post-money SAFEs affect dilution?

Post-money SAFEs fix the investor’s ownership percentage at the time of signing, so any dilution from additional SAFEs falls entirely on the founders and existing shareholders, not on the SAFE holder.

3. Do post-money SAFEs need a 409A valuation?

No, a 409A valuation is not required to issue a post-money SAFE. However, multiple SAFEs with low valuation caps can impact the company’s 409A valuation used to price stock options.

4. Can a post-money SAFE convert at a discount?

Yes, post-money SAFEs can include a discount rate, allowing the investor to convert at a reduced price compared to the priced round valuation, increasing their effective equity. However, this should be fixed at the time of agreement.

5. Are post-money SAFEs better for startups or investors?

Post-money SAFEs are more investor-friendly as they offer clear ownership percentages upfront. For startups, they simplify fundraising, but can result in greater founder dilution if not modeled correctly.