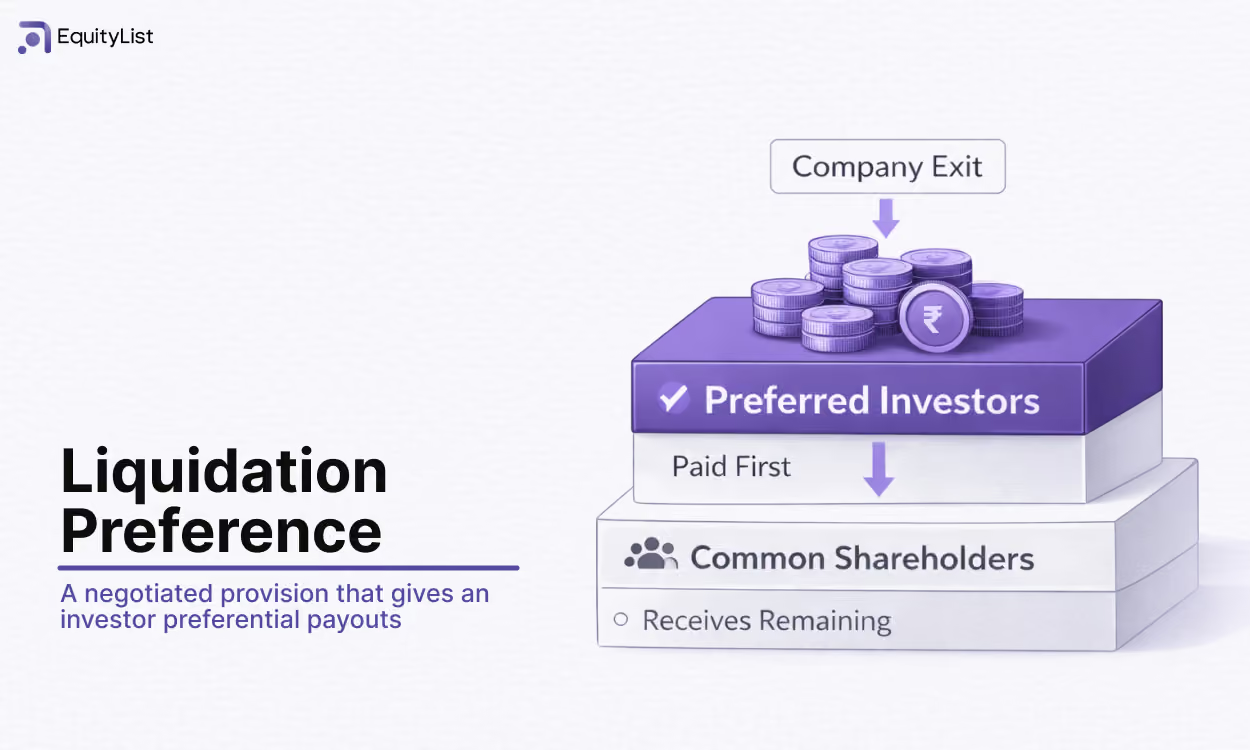

What is liquidation preference?

A liquidation preference is a contractual right that determines the order in which investors are paid when a company exits, whether through a sale, merger, asset sale, or liquidation.

It is typically granted to investors holding preference shares, giving them priority over founders, employees, and other common shareholders when exit proceeds are distributed.

This right is not automatic. It exists only when expressly set out in the Shareholders’ Agreement and reflected in the company’s Articles of Association.

How liquidation preference works

When a company exits, the sale proceeds are not distributed to all shareholders at once. Instead, they follow a fixed payout order, often referred to as a waterfall.

At a high level, exit proceeds are applied in the following sequence:

- Statutory dues and creditor obligations are settled first

- Investors with liquidation preference are paid next

- Any remaining amount is distributed to founders, employees, and other common shareholders

This ordering matters most in modest exits, where the total proceeds are not sufficient to fully cover all invested capital. In such cases, liquidation preference often determines whether common shareholders receive any payout at all.

The final distribution depends on how the liquidation preference is structured.

Types of liquidation preference

1. Liquidation multiplier

In a liquidation preference, the “x” refers to a multiple of the original investment that investors are entitled to receive before any proceeds are distributed to other shareholders.

- 1x liquidation preference means the investor gets back the amount they invested.

- 2x liquidation preference means the investor gets back twice their investment.

- 3x liquidation preference means the investor gets back three times their investment.

Only after this amount is paid does any remaining value flow to founders, employees, and other shareholders.

Higher multiples provide greater downside protection to investors, but they also increase the risk that founders and ESOP holders receive little or nothing in modest exits. For this reason, 1x liquidation preference remains the most common structure in venture deals.

2. Participating vs non-participating liquidation preference

This distinction often matters more than the multiple, because it determines whether investors are paid once or effectively paid twice in an exit.

a. Non-participating liquidation preference

Under a non-participating liquidation preference, the investor receives either their liquidation preference amount or their share of the exit proceeds based on ownership, whichever results in a higher payout.

If the investor gives up the liquidation preference, the preference shares are converted into ordinary (common) shares before the exit proceeds are distributed.

b. Participating liquidation preference

Under a participating liquidation preference, the investor:

- first receives their liquidation preference, and then

- also shares in the remaining proceeds in proportion to their ownership

This is often referred to as “double dipping”.

Participating preferences are uncommon in early-stage venture deals. They tend to appear in stressed situations or in later-stage rounds where founders have weaker negotiating leverage.

3. Seniority

When a company raises multiple funding rounds, there may be more than one group of investors with a liquidation preference. Seniority determines the order in which those preferences are paid.

Seniority is usually structured in one of two ways:

- Investor rounds may be treated pari passu, meaning all investors share the same seniority and are paid proportionately; or

- Through a stacked or senior preference structure, where investor rounds are paid in sequence, most commonly with later-stage investors paid first.

For example, assume a company raises $1M in Seed and $4M in Series A, with both investors holding a 1x liquidation preference.

If the company exits for $3M:

- Under a pari passu structure, Seed and Series A investors share the $3M proportionately.

- Under a stacked structure in which Series A is senior, Series A investors receive the entire $3M toward their 1x liquidation preference, and Seed investors receive nothing.

This is why stacked seniority increases risk for founders and early investors, particularly in down exits, even if the early capital was invested at a riskier stage.

Final takeaway

Liquidation preference is not about extreme outcomes or billion-dollar exits. It matters most in the far more common scenarios where a company exits below its headline valuation.

For founders, the key is not just the multiple, but how participation and seniority are structured across rounds. Two term sheets with the same valuation can lead to very different outcomes once liquidation preference is applied.

Understanding these mechanics early, and modelling realistic exit scenarios, is often more important than negotiating headline price alone.

FAQs

1. What is meant by liquidity preference?

“Liquidity preference” is often used interchangeably with “liquidation preference”. It refers to the same concept of deciding who gets paid first during an exit, such as a sale or merger.

2. What does a 2x liquidation preference mean?

A 2x liquidation preference means the investor is entitled to receive twice their invested amount before any proceeds are distributed to other shareholders.

If an investor invested $1M with a 2x liquidation preference, they are entitled to $2M first.

If the exit value is $1.5M, they take everything. Founders and employees receive nothing.